As of April 9, 2026 in India, the 8th Pay Commission implementation is entering its final discussion phase — and the latest news from employee union briefings confirms that the 2.86x fitment factor remains the government's working number, with the formal salary revision order expected before July 2026. For India's 1.18 crore central government employees, this is not just a salary hike — it is a complete recalculation of car loan eligibility, EMI capacity, and which vehicle segment is now affordable. Here is the complete 8th Pay Commission salary calculator breakdown and its direct impact on car loans.

8th Pay Commission Latest News: What Is the Implementation Date?

The 8th Pay Commission was constituted by the Union Cabinet in January 2025. As per the constitutional mandate and standard Pay Commission process, the implementation date is January 1, 2026 — meaning revised salaries apply from January 2026, though actual payment with arrears will happen after the formal order (expected June–July 2026). Key milestones:

- Constitution date: January 2025 (officially announced)

- Commission report submission: Expected March–April 2026

- Cabinet approval: Expected May–June 2026

- 8th Pay Commission implementation date: January 1, 2026 (retrospective)

- First revised salary credit: Expected July–August 2026 (with arrears)

- Arrear period: January 2026 to month of implementation — approximately 6–8 months

8th Pay Commission Salary Calculator: 2.86x Fitment Factor Results

The fitment factor is applied to the 7th CPC basic pay to arrive at 8th CPC basic pay. Here is the 8th Pay Commission salary calculator for major pay levels:

- Level 1 (7th CPC ₹18,000): 8th CPC at 2.86x → ₹51,480 basic | With DA 55%: ₹79,794 | Gross ~₹95,000/month

- Level 4 (7th CPC ₹25,500): 8th CPC → ₹72,930 basic | With DA: ₹1,13,041 | Gross ~₹1.30L/month

- Level 6 (7th CPC ₹35,400): 8th CPC → ₹1,01,244 basic | With DA: ₹1,56,928 | Gross ~₹1.75L/month

- Level 7 (7th CPC ₹44,900): 8th CPC → ₹1,28,414 basic | With DA: ₹1,99,042 | Gross ~₹2.20L/month

- Level 10 (7th CPC ₹56,100): 8th CPC → ₹1,60,446 basic | With DA: ₹2,48,691 | Gross ~₹2.75L/month

- Level 12 (7th CPC ₹78,800): 8th CPC → ₹2,25,368 basic | With DA: ₹3,49,320 | Gross ~₹3.80L/month

Note: Gross includes basic + DA (55%) + HRA (27% metro/18% non-metro/9% others) + transport allowance. These are planning figures; final numbers depend on city classification and individual pay matrix stage.

8th Pay Commission Employees Salary Hike: Car Loan Eligibility Impact

Banks calculate car loan eligibility at 3x–4x annual gross income, subject to EMI not exceeding 50% of net take-home. At a 7-year loan tenor and 8.5% interest rate:

- Level 1 employee (gross ~₹95K/month): 7th CPC loan eligibility: ~₹8L | 8th CPC loan eligibility: ~₹14–16L | Upgrade: Maruti Baleno → Tata Nexon EV base

- Level 4 employee (gross ~₹1.30L/month): 7th CPC: ~₹11L | 8th CPC: ~₹19–22L | Upgrade: Brezza ZXi → Nexon EV Max, Venue SX+

- Level 6 employee (gross ~₹1.75L/month): 7th CPC: ~₹15L | 8th CPC: ~₹25–30L | Upgrade: Creta base → Creta EV, Seltos HTX+

- Level 7 employee (gross ~₹2.20L/month): 7th CPC: ~₹19L | 8th CPC: ~₹32–38L | Upgrade: Seltos mid → Harrier EV, XUV700 AX7

- Level 10 employee (gross ~₹2.75L/month): 7th CPC: ~₹24L | 8th CPC: ~₹40–48L | Upgrade: Harrier petrol → Fortuner, Kodiaq, Gloster

8th Pay Commission Salary Hike + Company Lease: The Tax-Saving Double Benefit

Government employees can access cars through the Company Lease (Car Lease Policy) under the central government's LTC Cash Conversion or departmental vehicle lease schemes. This creates a tax-efficient structure that multiplies the 8th CPC salary hike benefit:

- How it works: The employer (ministry/department) leases the vehicle. EMI is deducted from salary before tax computation. The lease amount (typically ₹20,000–₹40,000/month for a mid-SUV) is treated as a perquisite valued at only 1.8% of car cost per year (for cars over ₹10L) — far lower than the actual lease cost

- Tax saved (Level 7 employee in 30% slab): Lease EMI ₹25,000/month × 12 = ₹3L/year. Taxable perquisite = 1.8% of ₹15L = ₹27,000. Tax on ₹27K vs tax on ₹3L: saving ~₹81,900/year in income tax

- At 8th CPC salary: More Level 7+ employees move into the 30% tax slab — making the lease tax saving even more valuable than under 7th CPC

January 2026 Arrears: Using It as Car Down Payment

The 8th Pay Commission arrears (January 2026 to implementation month) will be credited as a one-time lump sum. For a Level 6 employee:

- Monthly basic difference: ₹1,01,244 − ₹35,400 = ₹65,844

- With DA (55%): ₹65,844 × 1.55 = ₹1,02,057/month

- Over 7 months (Jan–Jul 2026): ₹7.14 lakh lump sum

- A ₹20L car requires 20% down payment = ₹4L — fully covered by arrears with ₹3.14L left over for road tax and insurance

This means a Level 6 government employee can buy a car in the ₹18–22L range without using any personal savings — the arrear alone covers the down payment and ancillary costs. Calculate your exact state road tax and registration charges first using our India on-road car price calculator so you know precisely how much of the arrear is needed.

🧮 Calculate On-Road Price Before Loan Application

Road tax ranges from 4% in Delhi to 13.5% in Karnataka. A ₹20L car costs ₹21.5L on-road in Delhi and ₹24L in Bengaluru. Know your number before the bank does.

8th Pay Commission Special Interest Rates: Banks Offering Deals This Month

Several banks have launched dedicated car loan schemes for government employees in anticipation of 8th Pay Commission salary revision — valid through April 2026:

- SBI Saral Car Loan (Govt Employees): 8.50% | Zero processing fee | Up to ₹25L | 7-year tenure | Salary account mandatory | EMI set at expected 8th CPC salary on submission of department letter

- Bank of Baroda Sarkari Vahan Yojana: 8.45% | No prepayment penalty | Joint application with spouse allowed | Max ₹25L

- Punjab National Bank Govt Car Loan: 8.55% | Up to 90% on-road funding | 7-year tenure | Special for employees with PNB salary account

- Canara Bank Central Pay Scheme: 8.60% | EMI up to 60% of gross | Available at all Canara branches with payroll relationship

- HDFC Bank Govt Advantage: 8.75% | 48-hour disbursal for Level 7 and above | 100% on-road funding available

8th Pay Commission Constitution: How It Affects You

The 8th Pay Commission was constituted under the resolution of the Union Cabinet — the same constitutional mechanism used for all prior pay commissions. It does not require parliamentary legislation. This means:

- The government can implement it by executive order (cabinet decision)

- Implementation from January 1, 2026 is assured — the only variable is the fitment factor (2.86x proposed vs 3.25x union demand)

- Even at the government's lower 2.86x proposal, the salary hike is the largest since the 7th CPC in 2016

- Defence, central police, and railway employees are covered — not just civil servants

For the official 8th Pay Commission terms of reference and constitution order, see the Department of Personnel & Training at dopt.gov.in. For tax implications of the arrear payment and how to claim Section 89(1) relief on the lump sum, the Income Tax India portal at incometax.gov.in has the Form 10E calculator.

FAQ: 8th Pay Commission and Car Loans

Can I apply for a car loan now based on expected 8th CPC salary?

Most PSU banks will not formally approve loans at revised salary before the cabinet order. However, you can apply at current 7th CPC salary — and once the order is issued and revised salary is credited, request a loan top-up or EMI revision without penalty under most government employee schemes. SBI Saral explicitly allows salary-revision-linked EMI adjustment.

Is the arrear amount taxable?

Yes — arrears are taxable as income in the year of receipt (FY 2026–27). File Form 10E on the Income Tax portal before filing your ITR to claim Section 89(1) relief, which spreads the tax liability across the years the arrear pertains to. This significantly reduces the effective tax on the lump sum — plan how much to earmark for a car down payment accordingly.

Frequently Asked Questions

Q: What is the current road tax rate for cars in India 2026?

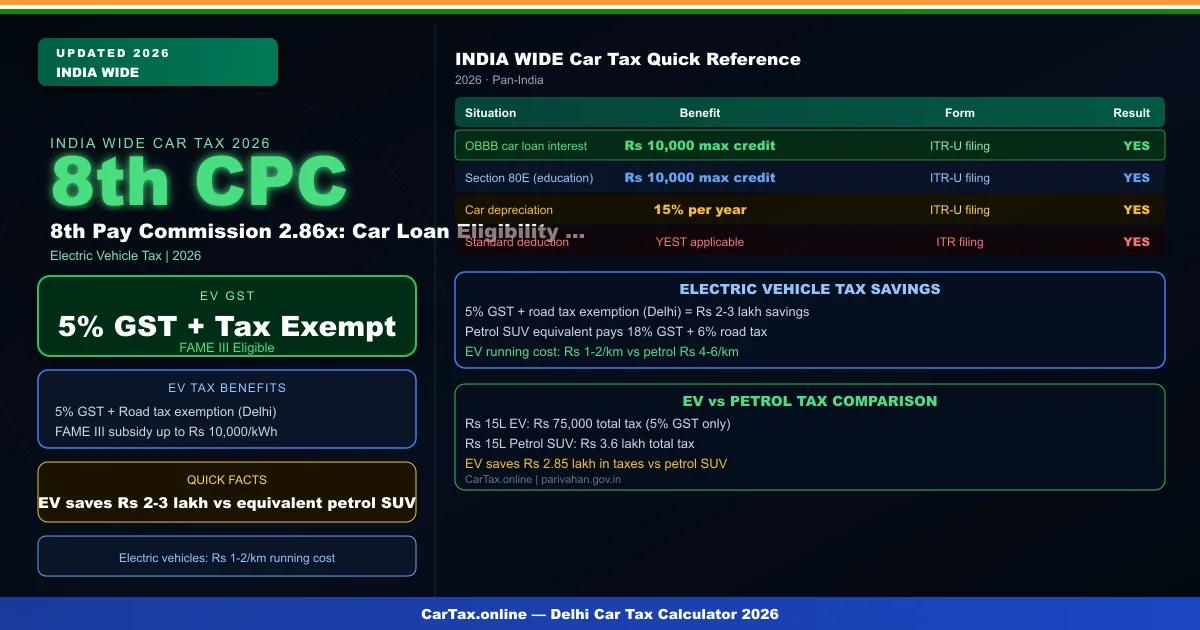

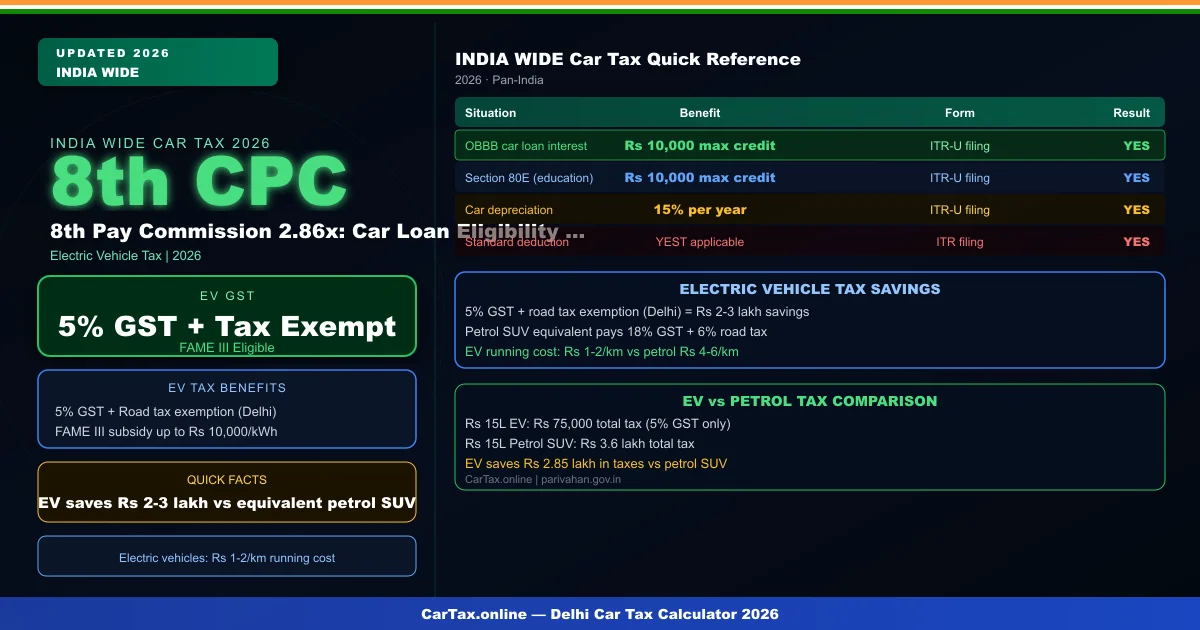

Road tax rates in India vary by state and vehicle category. For new cars, GST is charged at 5% for EVs, 18% for hybrids under 1,200cc, and up to 28% for petrol/diesel SUVs. State road tax is charged separately and varies from Rs3,000-15,000 annually depending on the state's slab system. Check your specific state's RTO website for current rates.

Q: How do I calculate my car road tax online in India?

You can calculate your car road tax using online calculators available on state RTO portals and CarTax.online. The calculation considers your vehicle's ex-showroom price, fuel type, engine capacity, and state of registration. Road tax is payable annually or for the vehicle's lifetime depending on your state's rules.

Q: Is GST included in the road tax for new cars in India?

No — GST and road tax are separate charges. GST is a central tax charged by the vehicle manufacturer at the time of purchase. State road tax is a separate annual or one-time charge levied by your state's transport department. Both apply at the time of first registration, and annual road tax continues for subsequent years.

Q: Do electric vehicles get tax benefits in India 2026?

Yes — electric vehicles in India qualify for a reduced GST rate of 5% (down from 28% for petrol cars). Under FAME-III subsidies, EVs may also qualify for additional state-level incentives, reduced road tax, and free registration in many states. The exact benefits vary by state.

Q: What happens if I don't pay my car road tax on time?

If you don't pay road tax, your vehicle's registration can be flagged in the Vahan database, preventing renewal of fitness certificates and creating legal liability during police checks. Penalties range from Rs200-500 per day of default in most states. Road tax is a legal requirement under the Motor Vehicles Act.