Starting April 1, 2026, a new 1% federal excise tax on cash remittances sent from the United States to foreign countries took effect under provisions of the One Big Beautiful Bill Act. As of April 7, 2026, millions of immigrant workers, expatriates, and families who regularly send money home through services like Western Union, MoneyGram, and Walmart2World are now paying more per transfer — specifically when using cash as the funding method. Here is exactly how the new tax works, who it affects, what is exempt, and the most cost-effective alternatives available today.

What Is the 1% Cash Remittance Tax?

The new Federal Remittance Excise Tax (FRET) — codified under OBBB Act Section 4475 — imposes a 1% tax on the total amount of any international money transfer that is funded using physical cash at the point of transaction. The key word is "cash" — the tax applies when you hand over dollar bills at a Western Union counter, a Walmart money services desk, a convenience store kiosk, or any agent location.

The tax is collected by the money transfer operator (MTO) at the time of transaction and remitted to the IRS quarterly. You will see it as a separate line item on your transfer receipt labeled "Federal Excise Tax" — distinct from the service fee and exchange rate spread that MTOs have always charged.

Exactly What Is Taxed — and What Is Not

The scope of the FRET is specifically limited to cash-funded transfers. The following are taxed:

- Physical cash paid at any MTO agent counter for international transfer

- Money orders purchased with cash and used to fund international transfers

- Cashier's checks funded from cash deposits specifically for remittance purposes (IRS Notice 2026-14 provides guidance)

The following are NOT taxed:

- Bank wire transfers (ACH or SWIFT) from a US bank account

- Transfers funded via debit card linked to a US bank account

- Transfers funded via credit card

- Digital app transfers where funds originate from a linked bank account (Wise, Remitly, Zelle to foreign accounts where applicable)

- Business-to-business wire transfers

- Transfers under $15 (de minimis threshold in the OBBB Act)

The tax is specifically designed to capture the informal cash economy of remittances — unbanked or under-banked senders who fund transfers in cash — while leaving the mainstream banking channel untouched.

Real Cost Impact: Before and After April 1, 2026

If you send $500 in cash to Mexico via Western Union, here is what the total cost looks like now versus before April 1:

- Western Union cash transfer fee (before April 1): $4.99 service fee + exchange rate spread (~1.2%) = total cost ~$11

- After April 1, 2026: $4.99 fee + 1% FRET ($5.00) + exchange rate spread = total cost ~$16

- Increase: $5 more per $500 sent — a 45% increase in total fees paid

For a family that sends $800/month to the Philippines:

- Monthly FRET cost: $8.00

- Annual FRET cost: $96/year in new federal tax alone

- Over 5 years: $480 in cumulative remittance tax

How to Legally Avoid the 1% Remittance Tax

The simplest way to avoid the FRET entirely is to not fund your international transfer with physical cash. Switching to any bank-linked digital method eliminates the tax. Here are the most cost-effective alternatives ranked by total cost for a $500 transfer to Mexico, India, or the Philippines (April 2026 rates):

- Wise (bank debit funding): ~$4.20 total fee + mid-market rate — no FRET. Best overall value for most corridors.

- Remitly Economy (bank debit): ~$3.99 fee — 3–5 business day delivery — no FRET. Cheapest for non-urgent transfers.

- Western Union bank account funding (online): Fee varies by corridor (~$0–$5) — no FRET on bank-funded transfers. Same brand, different funding = no tax.

- MoneyGram online (bank debit): ~$1.99–$4.99 — no FRET for bank-linked transfers.

- Zelle: No international transfers — domestic US only. Not applicable for remittances.

The practical takeaway: open a US bank account (even a basic free checking account) and fund all your remittances digitally. This saves the 1% FRET, typically also saves on service fees (online rates are often lower than in-person cash rates), and removes the need to carry large amounts of physical cash to a transfer agent.

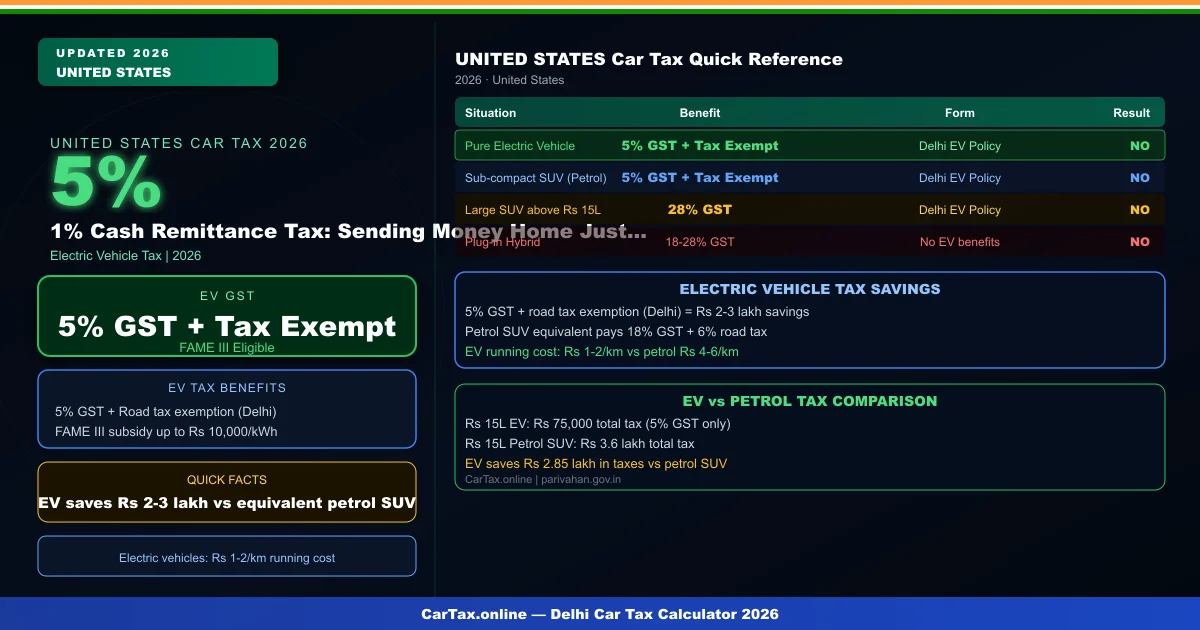

🚗 Stretch Your Savings Further: Car Tax Calculator

Whether you're buying a car in the US or back home in India or another country, use our calculators to understand the full tax cost before purchase.

Impact on Specific Communities

The communities most affected by the FRET are those with the highest cash remittance volumes — primarily Mexican, Indian, Filipino, Salvadoran, and Guatemalan diaspora communities in the United States. According to the World Bank, the US is the single largest source of global remittances, sending approximately $72 billion annually. If even 20% of that flow is cash-funded, the FRET generates approximately $144 million in annual federal revenue.

Advocacy groups including the National Immigration Forum and Center for Financial Services Innovation have flagged that the tax disproportionately burdens unbanked and under-banked immigrant workers — those least able to easily switch to digital banking channels. The OBBB Act does include a provision requiring the Treasury to publish a free guide to opening US bank accounts in 12 languages by June 2026 to facilitate the transition.

State-Level Remittance Taxes: A Note for California, New York, and Oklahoma Senders

The new federal 1% FRET comes on top of existing state-level remittance fees in some states. Oklahoma already charges a 1% state transfer tax on international remittances regardless of funding method. California and New York do not currently have state remittance taxes, but both states have pending legislation that could add 0.5–1% in 2027. If you are in Oklahoma, the combination of 1% state + 1% federal = 2% effective cash remittance tax as of April 2026.

Frequently Asked Questions

Does the 1% remittance tax apply to US citizens sending money abroad?

Yes — the FRET applies to any cash-funded international money transfer originating in the United States, regardless of the sender's citizenship or immigration status. US citizens sending cash remittances to family abroad are equally subject to the tax.

What happens if I use a prepaid debit card to fund a transfer?

Prepaid debit cards occupy a gray area in IRS Notice 2026-14. If the prepaid card was loaded with cash at a retail location (like a Green Dot card loaded at Walmart), the transfer may be classified as cash-funded and subject to FRET. If the prepaid card was loaded via ACH bank transfer, it is likely classified as bank-funded and exempt. The IRS has committed to issuing clarifying guidance on prepaid cards by July 2026. Until then, the safest approach is to use a traditional bank debit card for international transfers.

For the most current information on the Federal Remittance Excise Tax, check the IRS remittance tax guidance at irs.gov and IRS Notice 2026-14.

Frequently Asked Questions

Q: Can I deduct car payments on my taxes in 2026?

You cannot deduct car loan payments directly. However, you can deduct vehicle-related expenses if you use your car for business purposes — either through the standard mileage rate or by tracking actual expenses. The IRS allows Section 179 deductions for certain business vehicles up to their full purchase price.

Q: What is the federal tax credit for electric vehicles 2026?

The IRS Clean Vehicle Credit offers up to $7,500 for new EVs meeting domestic battery content requirements. Used EVs qualify for up to $4,000. Income limits and MSRP caps apply. Not all EVs qualify — check the IRS at irs.gov/cleanvehicle for the current list of eligible models.

Q: How does the IRS mileage rate work for car deductions?

The standard mileage rate for business use is 67 cents per mile for 2026. You can either use this flat rate (which includes depreciation) or track actual expenses including gas, insurance, repairs, and depreciation. The mileage method is simpler; the actual expense method is better for high-mileage drivers with expensive vehicles.

Q: Is sales tax on a car deductible?

Sales tax on a vehicle is not separately deductible if you use the standard deduction. However, if you itemize deductions and use your car for business, the sales tax may be partially included in your business use calculation. The IRS does not allow a direct deduction for sales tax on personal vehicle purchases.

Q: What records do I need for car tax deductions?

Keep a mileage log with date, destination, and business purpose for each trip. Save receipts for gas, insurance, repairs, and registration fees. Maintain your vehicle's purchase documents and depreciation records. The log should be maintained contemporaneously — a reconstructed log at tax time is not acceptable to the IRS.