As of April 8, 2026 in India, the gap between government and union positions on the 8th Pay Commission fitment factor has narrowed — but not closed. Employee unions are demanding 3.25x; the government's preliminary recommendations suggest 2.86x. For a central government employee deciding whether to buy a car today or wait for the announcement, this gap is the difference between a compact SUV and a mid-size SUV — literally. Here is the complete calculation of what each fitment factor means for your salary, loan eligibility, and whether January 2026 arrears can cover your down payment entirely.

8th Pay Commission Fitment Factor: Why 2.86x vs 3.25x Matters So Much

The fitment factor is the multiplier applied to 7th CPC basic pay to arrive at the revised 8th CPC basic pay. A higher multiplier means a higher basic pay, which cascades into Dearness Allowance (DA), HRA, travel allowance, and — most importantly for this discussion — gross income used to calculate car loan eligibility. Here is what the two scenarios mean at representative pay levels:

- Level 4 (7th CPC ₹25,500): At 2.86x → ₹72,930 | At 3.25x → ₹82,875 | Difference: ₹9,945/month

- Level 6 (7th CPC ₹35,400): At 2.86x → ₹1,01,244 | At 3.25x → ₹1,15,050 | Difference: ₹13,806/month

- Level 7 (7th CPC ₹44,900): At 2.86x → ₹1,28,414 | At 3.25x → ₹1,45,925 | Difference: ₹17,511/month

- Level 10 (7th CPC ₹56,100): At 2.86x → ₹1,60,446 | At 3.25x → ₹1,82,325 | Difference: ₹21,879/month

- Level 12 (7th CPC ₹78,800): At 2.86x → ₹2,25,368 | At 3.25x → ₹2,56,100 | Difference: ₹30,732/month

8th CPC Car Loan Eligibility: 2.86x vs 3.25x Scenarios

Banks calculate car loan eligibility on gross monthly income (basic + DA + HRA). Using standard public sector bank formula (60x monthly gross or 50% EMI-to-income, whichever is lower, at 8.5% for 7 years):

- Level 4 at 2.86x (gross ~₹1.25L/month): Max loan ₹18–22L → Nexon EV, Venue SX+, Tiago NRG

- Level 4 at 3.25x (gross ~₹1.42L/month): Max loan ₹22–26L → Nexon EV Max, Grand Vitara

- Level 6 at 2.86x (gross ~₹1.65L/month): Max loan ₹24–30L → Creta SX(O), Seltos HTX+

- Level 6 at 3.25x (gross ~₹1.88L/month): Max loan ₹28–35L → Harrier EV, XUV700

- Level 7 at 2.86x (gross ~₹2.05L/month): Max loan ₹30–38L → Scorpio N, Innova Hycross

- Level 7 at 3.25x (gross ~₹2.35L/month): Max loan ₹35–44L → Fortuner, Kodiaq

The fitment factor difference is a one-segment jump in purchasing power. At Level 6, the difference between 2.86x and 3.25x is the Hyundai Creta vs the Tata Harrier EV. Use our India on-road car price calculator to see road tax differences between states on these models — the Harrier EV qualifies for road tax exemption in Delhi, Maharashtra, and several other states, effectively reducing its on-road cost further.

January 2026 Arrears: Can You Buy a Car With Zero Down Payment?

If 8th CPC is implemented from January 1, 2026 (the expected date), and payments commence in mid-2026, government employees will receive approximately 6 months of arrears (January–June 2026) as a one-time lump sum. This is money that can directly fund a car down payment:

- Level 6 arrears at 2.86x: Monthly salary difference = ₹1,01,244 − ₹35,400 = ₹65,844. Over 6 months: ₹3.95L (basic only; with DA 55%: ₹65,844 × 1.55 × 6 = ₹6.12L)

- Level 6 arrears at 3.25x: Monthly difference = ₹1,15,050 − ₹35,400 = ₹79,650. Over 6 months with DA: ₹79,650 × 1.55 × 6 = ₹7.4L

- Level 7 arrears at 2.86x (with DA): ~₹7.75L one-time

- Level 7 arrears at 3.25x (with DA): ~₹9.1L one-time

The practical result: a Level 6 employee at 3.25x receives approximately ₹7.4L in arrears — enough to pay the down payment on a ₹20L car (20% = ₹4L) and still have ₹3.4L left for road tax and insurance. At 2.86x, the ₹6.12L arrear covers the down payment on the same car with less buffer but still without needing personal savings.

Should You Buy Now or Wait for the Fitment Announcement?

This is the real question. Key factors to consider:

- If you buy now at 7th CPC salary: Loan is approved at current salary. Once 8th CPC salary is credited, you can request a loan top-up or prepay from arrears — most PSU bank schemes allow this without penalty.

- If you wait: Risk of car price increases (Taigun Facelift, Toyota Ebella, and other April-May launches will set new price benchmarks). Also, GST rates are stable now — no announced changes.

- Strategic approach: Book a car today with the ₹25K–₹50K refundable token amount. Get loan pre-approval at current salary. When the 8th CPC order is issued (expected Q3 2026), renegotiate the loan amount with revised salary. The booking locks your price; the loan amount gets revised upward.

🧮 Calculate On-Road Price + Road Tax Before Applying for Loan

Your loan amount must cover the on-road price including road tax, registration, insurance. A ₹20L car in Karnataka has a ₹2.7L road tax — your loan must factor this in. Calculate it before you visit the bank.

PSU Bank Special Rates for 8th CPC Employees — April 2026

Several public sector banks have pre-emptively launched 8th CPC special car loan schemes, anticipating the salary revision:

- SBI Saral Car Loan (Govt): 8.50% interest | Zero processing fee | Loan up to ₹25L | EMI can be set at 40% of expected 8th CPC salary with revised salary certification

- Bank of Baroda Sarkari Vahan: 8.45% | No prepayment penalty | Joint application with spouse allowed | Loan up to ₹25L

- PNB Car Loan (Salary Account): 8.55% | Up to 90% on-road funding | Salary account mandatory | Lowest EMI among public sector options for Level 7+ employees

- Canara Bank Central Pay Scheme: 8.60% | Repayment up to 60% of gross | Available at all Canara branches with salary relationship

For tax implications of the arrear payment (Section 89 relief under the Income Tax Act), see the Income Tax India portal at incometax.gov.in — the Form 10E calculator is available there to estimate your tax liability and plan how much of the arrear to use for the car purchase.

Frequently Asked Questions

Q: What is the current road tax rate for cars in India 2026?

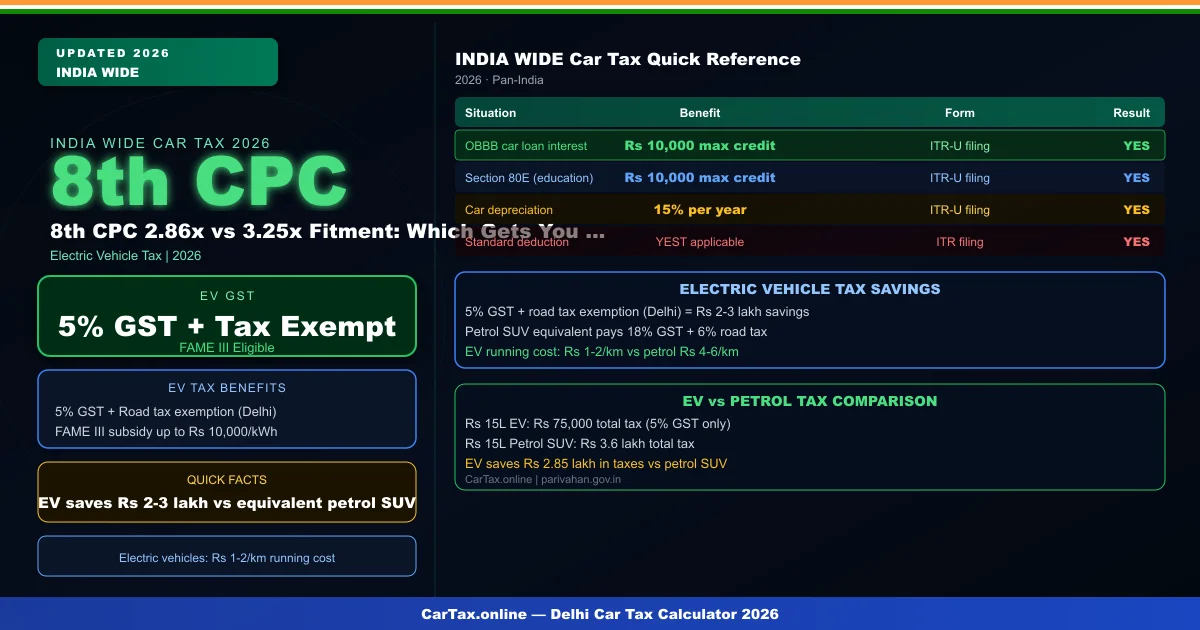

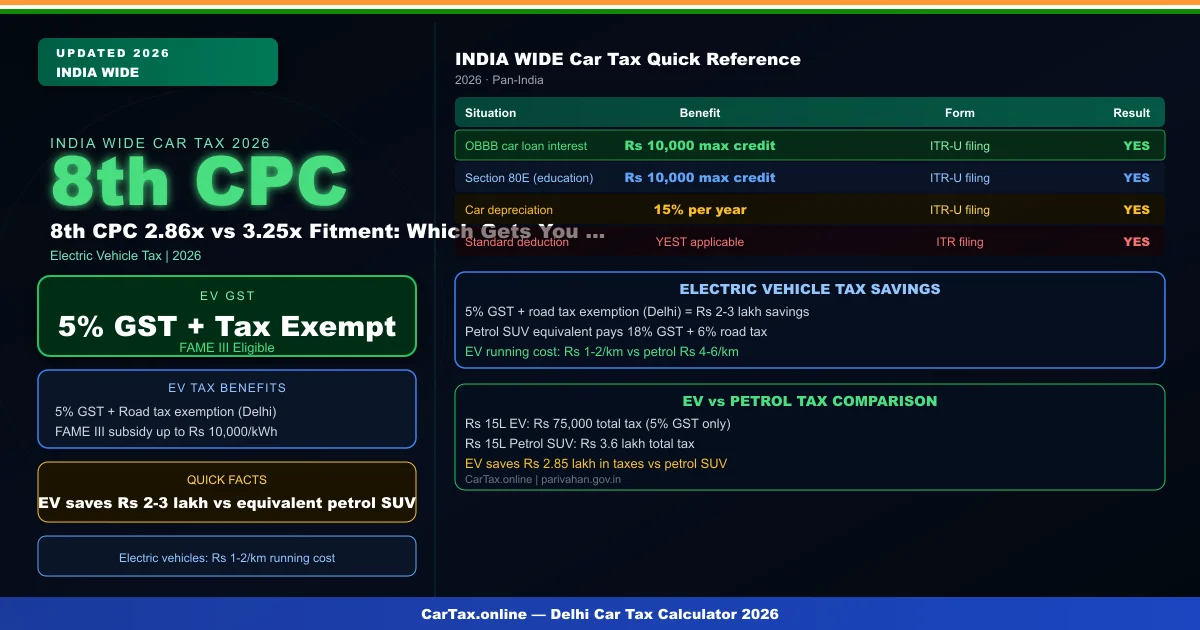

Road tax rates in India vary by state and vehicle category. For new cars, GST is charged at 5% for EVs, 18% for hybrids under 1,200cc, and up to 28% for petrol/diesel SUVs. State road tax is charged separately and varies from Rs3,000-15,000 annually depending on the state's slab system. Check your specific state's RTO website for current rates.

Q: How do I calculate my car road tax online in India?

You can calculate your car road tax using online calculators available on state RTO portals and CarTax.online. The calculation considers your vehicle's ex-showroom price, fuel type, engine capacity, and state of registration. Road tax is payable annually or for the vehicle's lifetime depending on your state's rules.

Q: Is GST included in the road tax for new cars in India?

No — GST and road tax are separate charges. GST is a central tax charged by the vehicle manufacturer at the time of purchase. State road tax is a separate annual or one-time charge levied by your state's transport department. Both apply at the time of first registration, and annual road tax continues for subsequent years.

Q: Do electric vehicles get tax benefits in India 2026?

Yes — electric vehicles in India qualify for a reduced GST rate of 5% (down from 28% for petrol cars). Under FAME-III subsidies, EVs may also qualify for additional state-level incentives, reduced road tax, and free registration in many states. The exact benefits vary by state.

Q: What happens if I don't pay my car road tax on time?

If you don't pay road tax, your vehicle's registration can be flagged in the Vahan database, preventing renewal of fitness certificates and creating legal liability during police checks. Penalties range from Rs200-500 per day of default in most states. Road tax is a legal requirement under the Motor Vehicles Act.