Vehicle Excise Duty (VED) — commonly referred to as road tax — is one of the oldest forms of taxation in the United Kingdom, dating back to the Vehicle Excise and Registration Act 1994. Understanding the legal framework behind VED helps drivers appreciate not just how much they pay, but why and how the system is administered. This guide covers the legislation, DVLA administration, enforcement powers, and how the VED system fits within the broader UK vehicle taxation framework for 2026.

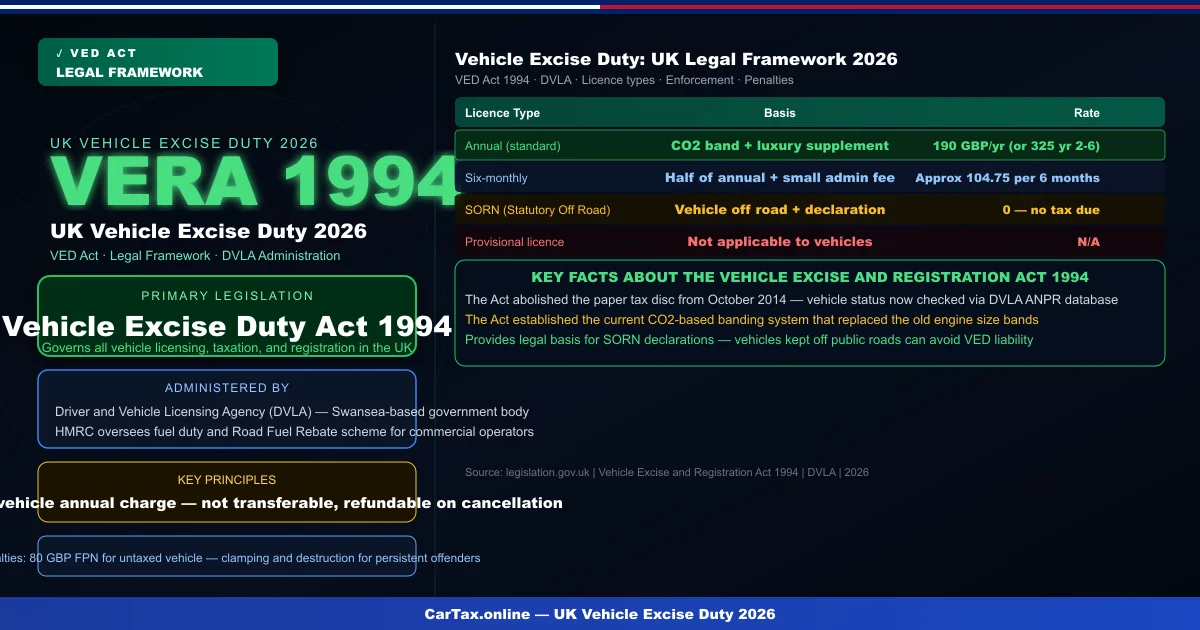

The Vehicle Excise and Registration Act 1994

The Vehicle Excise and Registration Act 1994 (VERA) is the primary legislation governing vehicle taxation in the United Kingdom. It consolidated previous road tax legislation and established the modern framework under which all vehicles must be licensed and taxed. The Act defines what vehicles are subject to VED, what exemptions apply, how the licensing system works, and the enforcement powers available to the DVLA. Key provisions include the abolition of the paper tax disc from October 2014 — since then, vehicle tax status is checked entirely via the DVLA's electronic database and ANPR camera network.

The CO2-based banding system

VERA 1994 was amended in 2009 to introduce the CO2-based banding system that replaced the previous engine-size classification for cars. Under this system, the VED rate for new cars depends on their CO2 emissions per kilometre at the point of first registration. The bands range from Band A (0-100g/km CO2, paying 0 first-year VED) through to Band M (226g/km+ CO2, paying the maximum 2,605 GBP first-year VED). This system was further reformed in 2022, when the first-year rates were simplified to a single standard rate applied to most cars from year 2 onwards, while the luxury supplement for vehicles with a list price over 40,000 GBP was introduced.

Who administers VED?

The Driver and Vehicle Licensing Agency (DVLA), based in Swansea, is responsible for administering VED in England, Scotland, and Wales. In Northern Ireland, vehicle licensing is administered by the Driver and Vehicle Agency (DVA). The DVLA maintains the vehicle registration database, issues vehicle registration certificates (V5C), processes road tax payments and refunds, and enforces VED compliance through its national field team and ANPR camera network. HMRC has a separate role in overseeing fuel duty — the duty charged on petrol, diesel, and other road fuels — which is a distinct charge from VED but related through the overall road funding system. Related: GST/HST Rebate on Vehicle Purchase 2026 | Canada Car Import Duty 2026 | Canada Vehicle CCA Depreciation 2026 | Car Import Tax India 2026.

Licence types under VERA 1994

The Act defines several types of vehicle licence. The standard annual licence is the most common — payable yearly, six-monthly, or by monthly Direct Debit for most vehicles. The Act also provides for SORN (Statutory Off Road Notification) licences, which suspend the road tax liability while a vehicle is kept off public roads. There are also provisions for short-term licences, trade licences for garages and dealers, and special exemption categories for historic vehicles, disabled persons, and agricultural vehicles. The Act was amended to provide for the 5-year VED exemption for pure electric vehicles registered from April 2017.

Enforcement powers

VERA 1994 gives the DVLA significant enforcement powers. These include the authority to issue Fixed Penalty Notices (FPN) of 80 GBP (reduced to 40 GBP if paid within 36 days) for untaxed vehicles, to clamp and remove untaxed vehicles, and to dispose of vehicles that remain untaxed and unclaimed. The DVLA's field enforcement teams operate nationally, identifying untaxed vehicles through a combination of ANPR camera data and physical patrols. Vehicles clamped for being untaxed on a public road incur a release fee of 95 GBP, and vehicles not released within 24 hours of clamping are taken to a storage facility at a cost of 22 GBP per day.

Penalties for non-payment

- First detection: 80 GBP Fixed Penalty Notice (40 GBP if paid within 36 days)

- Clamping: removal free to DVLA, 95 GBP release fee to vehicle owner

- Impound storage: 22 GBP per day after first 24 hours

- Destruction: owner pays all costs if vehicle not reclaimed

- No valid defences: even vehicles awaiting tax renewal are not exempt from penalty

How road tax fits into UK transport funding

It is a common misconception that road tax funds roads. In fact, VED revenue goes directly to the Treasury's consolidated fund rather than being ring-fenced for road maintenance or construction. Roads are funded from general taxation through the Department for Transport's national roads fund and local authority highway maintenance budgets. Fuel duty — currently 57.95p per litre for both petrol and diesel — is also not ring-fenced despite being historically presented as a road-funded charge. This means drivers effectively pay twice for road use: once through VED and again through fuel duty and other taxation.

Amendments and reforms since 1994

The Vehicle Excise and Registration Act 1994 has been amended numerous times. The 2009 reforms introduced CO2-based banding. The 2017 reforms introduced the diesel surcharge and luxury vehicle supplement, while also introducing the 5-year VED exemption for pure electric vehicles. The 2022 reforms simplified the annual VED structure by replacing the complex graduated annual rates with the current standard 190 GBP annual rate. Future reforms under consideration include a review of the electric vehicle VED exemption, a potential per-mile road pricing scheme for post-2027, and adjustments to the luxury vehicle price threshold.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. VED legislation is subject to change. For the most current legal references, consult legislation.gov.uk and gov.uk/vehicle-tax. Rates and regulations reflect April 2026 government policy.

Official Resources: Vehicle Tax Guide | Car Tax Calculator

Frequently Asked Questions

Q: How is car tax calculated in 2026?

Car tax is calculated based on your vehicle's value, engine capacity, fuel type, emissions, and state or country of registration. Tax rates vary significantly between regions — check your local transport authority website or use an online car tax calculator for an accurate estimate for your specific vehicle.

Q: Can I pay my car tax online?

Yes — most regions allow online road tax payment through their transport department portal. In India, use parivahan.gov.in. In the UK, use gov.uk. In the USA, check your state's DMV website. Have your vehicle registration number and insurance certificate ready for online payments.

Q: What happens if I don't pay car tax?

Driving without valid road tax is illegal in most jurisdictions and can result in fines, vehicle seizure, or number plate clamping. Penalties range from a percentage of the tax owed to fixed daily amounts. Always ensure your vehicle is taxed before driving — even short lapses can accumulate significant penalties.

Q: Are there tax exemptions for electric or hybrid vehicles?

Most countries offer tax benefits for EVs and hybrids including reduced GST/VAT rates, road tax exemptions, and purchase subsidies. In India, EVs attract 5% GST versus 28% for petrol cars. In the UK, EVs are exempt from VED. Check your country's specific EV incentive programs for current rates and eligibility.

Q: Can I claim tax relief on car expenses for business use?

Business vehicle owners can typically claim deductions for fuel, maintenance, insurance, depreciation, and interest on car loans. Methods vary: standard mileage rates, actual expense tracking, or lease deduction. Keep detailed records including mileage logs, receipts, and business purpose documentation for all trips.