Performance car insurance is among the most expensive categories of motor cover in the UK market, with annual premiums for high-powered sports cars often reaching 1,500 to 3,000 GBP and exceeding 5,000 GBP for the most powerful supercars. Understanding how insurers assess performance risk and what steps owners can take to reduce premiums is essential for anyone considering a performance vehicle.

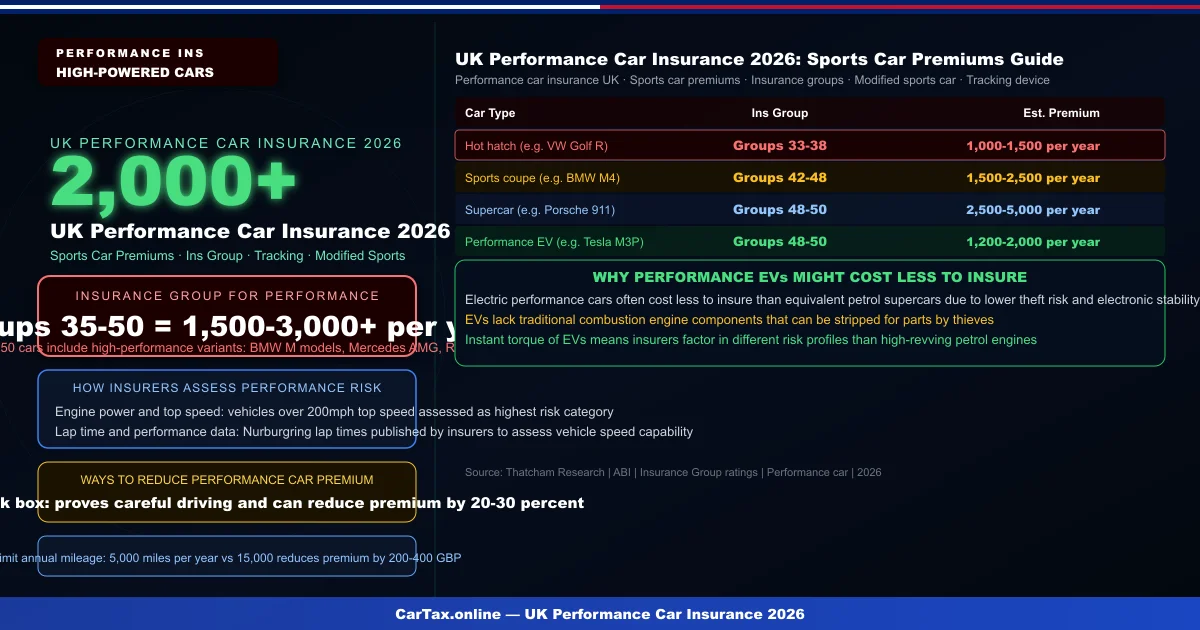

Insurance Groups for Performance Cars

UK car insurance groups range from Group 1 (lowest risk) to Group 50 (highest risk). Performance cars typically fall into Groups 35 to 50, with the highest-powered variants of BMW M models, Mercedes-AMG, Audi RS, Porsche 911 and similar vehicles occupying the top groups. The insurance group is determined by factors including engine power, top speed, performance capability and theft risk.

Hot hatches such as the VW Golf R (Groups 33 to 38) typically cost 1,000 to 1,500 GBP per year to insure. Sports coupes such as the BMW M4 (Groups 42 to 48) range from 1,500 to 2,500 GBP per year. Full supercars such as the Porsche 911 (Groups 48 to 50) can cost 2,500 to 5,000 GBP per year.

How Insurers Assess Performance Risk

Insurers assess performance vehicles using multiple risk factors beyond standard criteria. Engine power and acceleration statistics are primary rating factors, with vehicles capable of 0-60 mph in under four seconds assessed as highest risk. Top speed is a significant factor, with vehicles over 200 mph theoretical top speed in the highest risk category. Insurers increasingly use published performance data, including Nurburgring lap times, as proxies for real-world driving behaviour risk. Related: Canada Car Insurance Tax 2026 | Car Insurance Tax India 2026 — GST & Income Tax Benefits | Car Insurance UAE 2026 | Auto Insurance Uk.

Modifications that increase performance, even if well-intentioned, typically increase premiums by 10 to 30 percent because they are perceived as increasing the vehicle's speed capability and therefore risk profile. Even approved manufacturer performance variants (M Sport, AMG Line, S-Line) are rated higher than standard versions of the same base model.

Ways to Reduce Performance Car Insurance Premiums

Telematics black box policies are particularly effective for performance car owners aged under 50, offering 20 to 30 percent premium reductions for careful drivers who can demonstrate low-speed, smooth driving patterns. Limiting annual mileage to 5,000 miles per year versus 15,000 can reduce premiums by 200 to 400 GBP. Installing Thatcham-approved security devices, including S5 GPS trackers, can provide additional discounts of 10 to 20 percent.

Performance electric vehicles such as the Tesla Model 3 Performance, while sharing high insurance groups with petrol supercars, sometimes benefit from lower theft rates and electronic stability systems that insurers factor into their risk models. Premiums for performance EVs typically range from 1,200 to 2,000 GBP, lower than equivalent-performance petrol cars.

Frequently Asked Questions

Why is performance car insurance so expensive? Performance cars are statistically more likely to be involved in serious accidents due to their power and the driving profiles of their owners. They are also more likely to be stolen, particularly high-value sports cars, and more expensive to repair using manufacturer-approved parts.

Do performance EVs cost less to insure than petrol supercars? Often yes. Performance EVs such as the Tesla Model 3 Performance can cost 1,200 to 2,000 GBP per year, compared to 2,500 to 5,000 GBP for equivalent-performance petrol supercars, partly due to lower theft rates and advanced electronic stability systems.

Official Resources: GOV.UK Check Vehicle Tax | GOV.UK Vehicle Tax | DVLA Online | MOT Check

Frequently Asked Questions

Q: How much is car tax (VED) in the UK 2026?

Car tax rates in the UK depend on your vehicle's CO2 emissions and list price. Standard rates start from £190 per year for petrol and diesel cars, with zero-rated VED for EVs. First-year rates vary from £0 to £2,605 depending on emissions. Additional premiums apply for vehicles over £40,000.

Q: How do I check if my car is taxed online?

You can check your vehicle's tax status for free on the Gov.uk website at gov.uk/check-vehicle-tax. You'll need your vehicle's registration number (number plate). You can also check via the Motor Insurance Database to verify road tax and insurance status simultaneously.

Q: Can I get a refund on car tax if I sell my vehicle?

Yes — if you sell or scrap your vehicle, you can claim a refund on any full months of remaining road tax. Contact DVLA with the V11 reminder letter or apply online at gov.uk. Refunds are usually processed within 4-6 weeks.

Q: Is road tax refund available when transferring ownership?

No — road tax does not transfer with the vehicle. When you sell your car, the tax is automatically cancelled and any remaining months are refunded to you by DVLA. The new owner must tax the vehicle immediately. As a buyer, always verify the vehicle's tax status before purchasing.

Q: What is the luxury car tax threshold in the UK 2026?

The additional rate for vehicles over £40,000 (list price) adds £410 per year to standard VED rates for years 2-6 of registration. This surcharge brings the annual cost for high-emission vehicles over £40,000 to around £600-690 per year. Pure EVs under £40,000 pay zero VED.