Auto insurance UK is a legal requirement for all vehicle owners. Driving without valid motor insurance carries fines of up to 5,000 GBP, vehicle seizure and potential disqualification from driving. Understanding the types of cover available, what affects your premium and how to reduce costs can save hundreds of pounds annually.

Types of Auto Insurance Cover in the UK

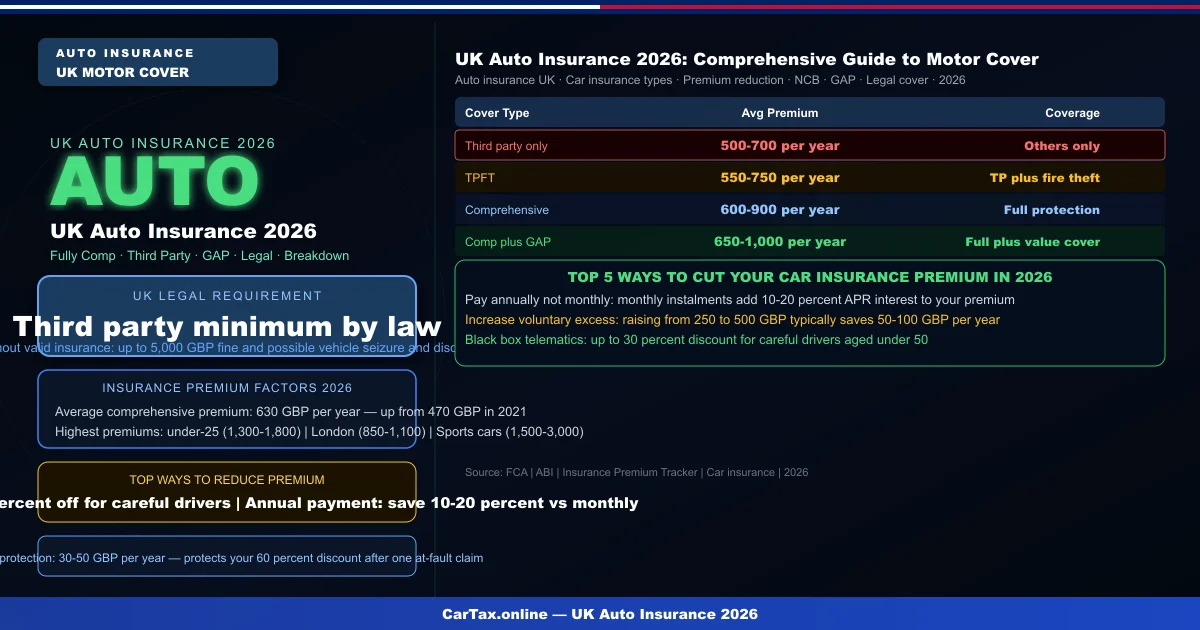

Third Party Only (TPO)

The minimum legal requirement in the UK. TPO covers damage you cause to other people, their vehicles and property, but does not cover any damage to your own vehicle. Annual premiums average 500 to 700 GBP. This cover is rarely cost-effective for newer cars but suits older, low-value vehicles where the premium difference between TPO and comprehensive is small.

Third Party, Fire and Theft (TPFT)

Adds cover for your vehicle being stolen or destroyed by fire on top of the third party minimum. Costs approximately 50 to 100 GBP more per year than TPO on average. This is a middle-tier option but comprehensive cover typically costs only slightly more while providing substantially better protection.

Comprehensive Cover

The fullest level of protection, covering damage to your vehicle in accidents (regardless of fault), fire, theft, vandalism and windscreen damage. Average annual comprehensive premium is 630 GBP in 2026. Surprisingly, comprehensive cover is often only 30 to 80 GBP more per year than TPFT, making it the clear value choice for most drivers. Related: UK Car Insurance Guide 2026 | UK Car Insurance Types 2026 | UK Insurance Add-ons 2026 | UK Insurance No Claims Bonus 2026.

What Affects Your Auto Insurance Premium in 2026

Insurers use risk profiling based on multiple factors. Key premium drivers include your age and experience, with under-25 drivers paying the highest premiums (1,300 to 1,800 GBP per year) due to accident statistics. Location matters significantly, with London averaging 850 to 1,100 GBP per year versus national averages. Vehicle type and insurance group (1 to 50) directly affect premiums, with high-performance and sports cars commanding the highest rates.

Annual mileage is a key factor: 5,000 miles per year versus 15,000 can reduce premium by 200 to 400 GBP. Driving history, including claims and convictions, affects premiums for three to five years. Your job title is used as a risk proxy and can affect quotes by hundreds of pounds. Credit history increasingly influences insurance pricing alongside other factors.

Ways to Reduce Your Auto Insurance Premium

Pay annually rather than monthly: spreading payments adds 10 to 20 percent in APR interest charges. Increasing voluntary excess from 250 to 500 GBP can save 50 to 100 GBP per year. Telematics black box policies offer 20 to 30 percent discounts for careful drivers, particularly beneficial for under-25s. Restricting drivers to named policyholders only, rather than open policies, reduces costs.

Installing Thatcham-approved security devices can reduce premiums by 7 to 15 percent. Parking off-road overnight versus on-street parking can reduce premiums by 100 to 300 GBP annually. Building a No Claims Bonus (NCB) over five-plus years provides the most significant long-term reduction, reaching 60 to 70 percent discount at maximum NCB level.

No Claims Bonus and Protection

Your No Claims Bonus (NCB) is one of the most valuable assets in reducing car insurance costs. Each claim-free year adds one year to your NCB. After five years, you can protect your NCB, typically costing 30 to 50 GBP per year, which allows you to make one claim without losing your NCB. Maximum NCB is typically five to seven years depending on insurer.

GAP Insurance Explained

GAP (Guaranteed Asset Protection) insurance covers the difference between your car's market value and the amount you owe on finance or its original purchase price if written off. In 2026, new cars can lose 40 to 50 percent of their value in the first three years, potentially leaving owners thousands of pounds out of pocket on a financed vehicle. GAP policies cost 150 to 300 GBP per year when bought standalone, versus 200 to 500 GBP as a dealer add-on.

Legal Cover Add-Ons

Legal expenses cover included in many comprehensive policies pays for solicitor fees if you need to make or defend a personal injury or uninsured loss claim following an accident. Motor legal protection typically costs 20 to 50 GBP when purchased standalone but is often included free with comprehensive cover. It is particularly valuable when the other driver is uninsured or disputes liability.

Frequently Asked Questions

Is third party insurance actually cheaper than comprehensive? Not necessarily. The premium difference is often only 30 to 80 GBP per year. Given comprehensive cover protects your vehicle as well as others, it almost always offers better value.

Do I need car insurance before buying a car? Yes. You cannot drive a car on public roads without insurance, even to bring it home from the dealership. Most insurers offer immediate cover via phone or app.

How long does a claim stay on my insurance? At-fault claims typically remain on your record for five years and affect premiums. Non-fault claims are recorded for two to three years. Conviction points affect insurance for four to five years.

Can I transfer my No Claims Bonus to another car? Yes. Your NCB belongs to you as a driver, not to a specific vehicle. It can be transferred between cars and, if you have two cars, you can split NCB across both policies.

What should I do after a car accident? Exchange details with all parties, take photos, get witness details, report to your insurer within 24 to 48 hours, and complete an accident report form. Do not admit fault at the scene.

Official Resources: Parivahan Portal | Vahan Road Tax | India GST Portal | FAME-III Scheme

Frequently Asked Questions

Q: What is the current road tax rate for cars in India 2026?

Road tax rates in India vary by state and vehicle category. For new cars, GST is charged at 5% for EVs, 18% for hybrids under 1,200cc, and up to 28% for petrol/diesel SUVs. State road tax is charged separately and varies from Rs3,000-15,000 annually depending on the state's slab system. Check your specific state's RTO website for current rates.

Q: How do I calculate my car road tax online in India?

You can calculate your car road tax using online calculators available on state RTO portals and CarTax.online. The calculation considers your vehicle's ex-showroom price, fuel type, engine capacity, and state of registration. Road tax is payable annually or for the vehicle's lifetime depending on your state's rules.

Q: Is GST included in the road tax for new cars in India?

No — GST and road tax are separate charges. GST is a central tax charged by the vehicle manufacturer at the time of purchase. State road tax is a separate annual or one-time charge levied by your state's transport department. Both apply at the time of first registration, and annual road tax continues for subsequent years.

Q: Do electric vehicles get tax benefits in India 2026?

Yes — electric vehicles in India qualify for a reduced GST rate of 5% (down from 28% for petrol cars). Under FAME-III subsidies, EVs may also qualify for additional state-level incentives, reduced road tax, and free registration in many states. The exact benefits vary by state.

Q: What happens if I don't pay my car road tax on time?

If you don't pay road tax, your vehicle's registration can be flagged in the Vahan database, preventing renewal of fitness certificates and creating legal liability during police checks. Penalties range from Rs200-500 per day of default in most states. Road tax is a legal requirement under the Motor Vehicles Act.