April 13, 2026 in United Kingdom — The Zero Emission Vehicle (ZEV) mandate is reshaping the UK car market and directly affecting Vehicle Excise Duty rates. Understanding how this government policy impacts your car tax is essential whether you are buying a new vehicle or planning a fleet transition in 2026.

Understanding the UK ZEV Mandate

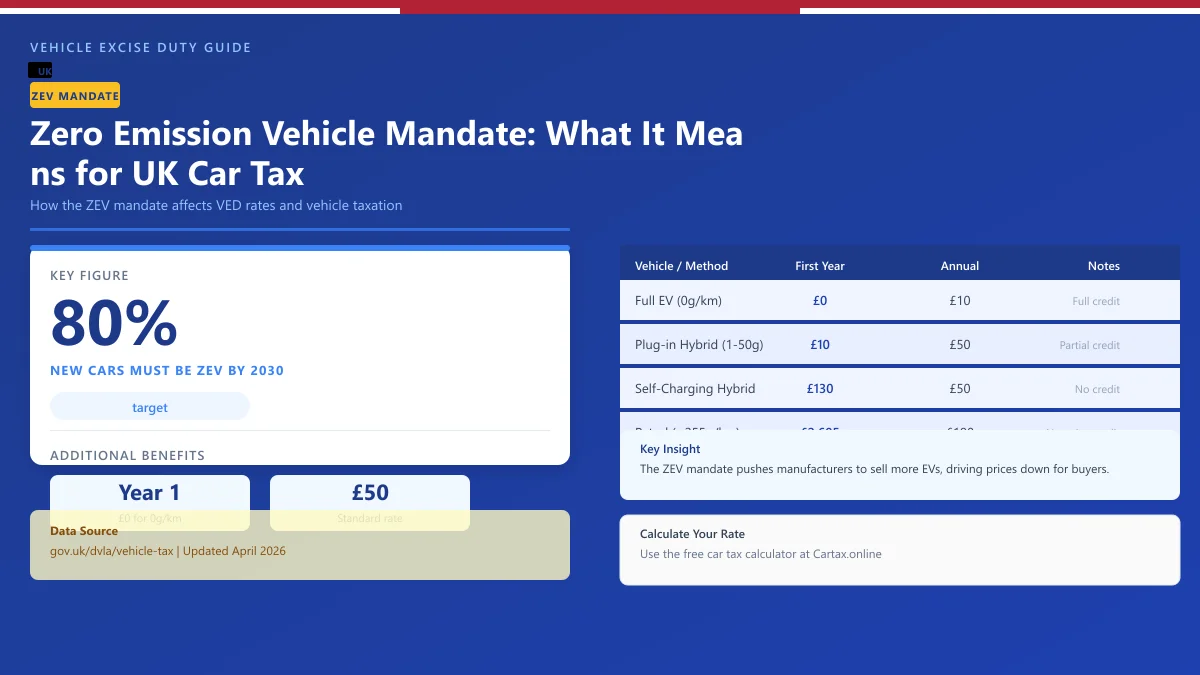

The Zero Emission Vehicle mandate requires manufacturers to sell an increasing percentage of zero-emission cars and vans each year. By 2030, the target is 80% of new car sales being zero-emission. This regulatory framework directly impacts vehicle taxation because low and zero-emission vehicles receive preferential VED rates.

The mandate creates a financial incentive structure where manufacturers who exceed their ZEV targets can sell credits to those who fall short, effectively cross-subsidising the production of affordable EVs. The zero emission vehicle mandate UK therefore has a direct effect on car tax — as EV production scales up, prices fall, making zero-emission vehicles accessible to more buyers.

ZEV Mandate and VED: How It Affects Your Car Tax

All zero-emission vehicles registered from April 2025 pay £0 first-year VED, then £10 annual rate for years 2-6, and the standard rate thereafter. This contrasts with petrol cars emitting over 255g/km of CO2, which pay £2,605 in year one: Related: Zero Emission Vehicle Mandate UK 2026 | UK Zero Emission Vehicle Tax 2026 | Zero Emission Car Tax UK 2026 | Zero Emission Car Tax UK 2026.

- Full EV (0g/km): £0 first year, £10 annually (years 2-6) — full ZEV credit

- Plug-in Hybrid (1-50g/km): £10 first year, £50 annually — partial ZEV credit

- Self-Charging Hybrid: £130 first year, £50 annually — no ZEV credit

- Petrol (130g/km): £205 first year, £190 annually — zero ZEV credit

- Petrol (>255g/km): £2,605 first year, £190 annually — negative ZEV credit

How the ZEV Mandate Affects Plug-in Hybrid Tax

Plug-in hybrids (PHEVs), which combine a petrol engine with an electric motor and emit between 1-50g/km, have faced shrinking incentive structures. Under the current VED rules from April 2025, PHEVs still qualify for the £10 first-year rate, but the benefit-in-kind rates for company car drivers have been reduced to narrow the gap with full EVs.

The zero emission vehicle mandate UK effectively pushes manufacturers away from PHEVs and toward full battery electric vehicles (BEVs), because PHEVs count at a reduced rate toward the manufacturer's ZEV sales quota. This is changing the vehicle market as manufacturers phase out plug-in hybrid models in favour of full EVs.

Second-hand EV Market and Tax Implications

The ZEV mandate primarily affects new car sales, but the downstream effect on the used market is significant. As new EV prices fall due to manufacturer compliance with ZEV targets, used EV prices are also declining, making them more accessible to budget-conscious buyers.

A used electric vehicle (first registered before April 2025) pays the same annual VED as a new EV — currently £10 for years 2-6, then the standard rate. The low tax burden is one of the key advantages of buying an EV, regardless of age. This means buying a second-hand EV gives you the ongoing zero emission vehicle mandate UK tax benefits at a significantly reduced purchase price.

Preparing for the 2030 ZEV Target

By 2030, it is expected that 100% of new car sales will be zero-emission. For car buyers, this means the VED landscape will look very different — most vehicles on the road will attract minimal road tax, and the revenue base for the government will shift toward other forms of motoring taxation such as road user charging.

The transition strategy for buyers is clear: EVs offer the lowest total cost of ownership when fuel savings, maintenance reductions, and VED savings are combined. The upfront purchase premium is decreasing as manufacturer compliance with the ZEV mandate drives down prices.

Conclusion

The zero emission vehicle mandate UK is transforming car tax. EVs pay £0 first-year VED and just £10 annually for years 2-6. As the 2030 ZEV target approaches, prices are falling and used EV availability is growing. Use our car tax calculator to compare VED rates for electric vs petrol vehicles and plan your next purchase. Read more at GOV.UK ZEV mandate guidance.

Frequently Asked Questions

Q: How much is car tax (VED) in the UK 2026?

Car tax rates in the UK depend on your vehicle's CO2 emissions and list price. Standard rates start from £190 per year for petrol and diesel cars, with zero-rated VED for EVs. First-year rates vary from £0 to £2,605 depending on emissions. Additional premiums apply for vehicles over £40,000.

Q: How do I check if my car is taxed online?

You can check your vehicle's tax status for free on the Gov.uk website at gov.uk/check-vehicle-tax. You'll need your vehicle's registration number (number plate). You can also check via the Motor Insurance Database to verify road tax and insurance status simultaneously.

Q: Can I get a refund on car tax if I sell my vehicle?

Yes — if you sell or scrap your vehicle, you can claim a refund on any full months of remaining road tax. Contact DVLA with the V11 reminder letter or apply online at gov.uk. Refunds are usually processed within 4-6 weeks.

Q: Is road tax refund available when transferring ownership?

No — road tax does not transfer with the vehicle. When you sell your car, the tax is automatically cancelled and any remaining months are refunded to you by DVLA. The new owner must tax the vehicle immediately. As a buyer, always verify the vehicle's tax status before purchasing.

Q: What is the luxury car tax threshold in the UK 2026?

The additional rate for vehicles over £40,000 (list price) adds £410 per year to standard VED rates for years 2-6 of registration. This surcharge brings the annual cost for high-emission vehicles over £40,000 to around £600-690 per year. Pure EVs under £40,000 pay zero VED.