Car tax conversion UK — vehicles that have been converted from one fuel type to another, or substantially modified, have specific VED rules. Here is how road tax applies to converted vehicles in 2026.

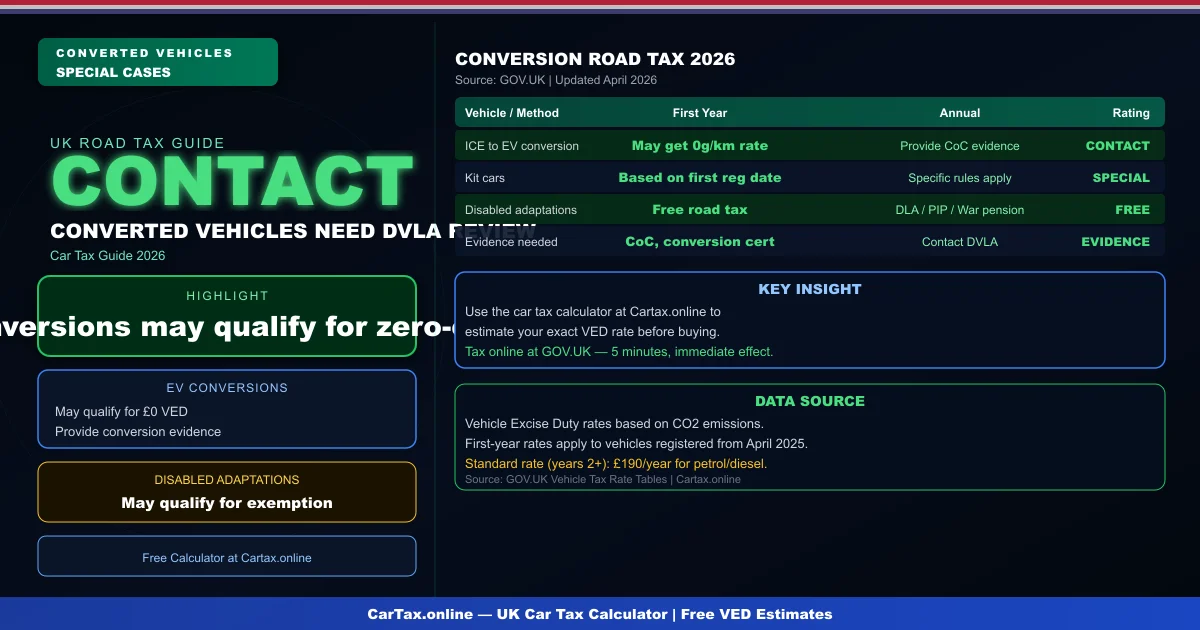

ICE to EV Conversions

Converting an internal combustion engine (ICE) vehicle to electric power does not change the vehicle's road tax classification automatically. The converted vehicle retains its original first registration date — and therefore may retain some characteristics of the original vehicle's tax class. Contact DVLA to understand how your specific conversion will be classified for VED purposes.

How VED Is Calculated for Conversions

When a vehicle is converted, DVLA may reclassify it based on the new CO2 figure if the conversion has changed the vehicle's emissions. A converted EV (0g/km) may qualify for the zero-emission VED rate if DVLA accepts the new CO2 data. You will need to provide evidence of the conversion and updated CO2 certification.

Kit Cars and VED

Kit cars — where a vehicle is assembled from a kit — may have a different first registration date and tax classification from the original kit components. The tax class is based on the date the completed vehicle is first registered, not the date the kit was manufactured. DVLA has specific rules for kit car VED classification. Related: Car Tax Conversion UK 2026 | Car Tax for Conversion Vehicles UK 2026 | Ev Conversion Uk | Car Tax for Conversion Vehicles UK 2026.

Adapted Vehicles for Disability

Vehicles adapted for disabled drivers or passengers may qualify for reduced or zero road tax. Vehicles used by disabled people who receive the mobility component of the Disability Living Allowance (DLA), Personal Independence Payment (PIP), or War Pensioners' Mobility Supplement may qualify for free road tax. Apply using the relevant documentation to DVLA.

Conclusion

Car tax conversion UK: converted EVs may qualify for zero-emission VED. Kit cars have specific rules. Adapted vehicles may qualify for disability exemption. GOV.UK has full conversion vehicle guidance.

Frequently Asked Questions

Q: How much is car tax (VED) in the UK 2026?

Car tax rates in the UK depend on your vehicle's CO2 emissions and list price. Standard rates start from £190 per year for petrol and diesel cars, with zero-rated VED for EVs. First-year rates vary from £0 to £2,605 depending on emissions. Additional premiums apply for vehicles over £40,000.

Q: How do I check if my car is taxed online?

You can check your vehicle's tax status for free on the Gov.uk website at gov.uk/check-vehicle-tax. You'll need your vehicle's registration number (number plate). You can also check via the Motor Insurance Database to verify road tax and insurance status simultaneously.

Q: Can I get a refund on car tax if I sell my vehicle?

Yes — if you sell or scrap your vehicle, you can claim a refund on any full months of remaining road tax. Contact DVLA with the V11 reminder letter or apply online at gov.uk. Refunds are usually processed within 4-6 weeks.

Q: Is road tax refund available when transferring ownership?

No — road tax does not transfer with the vehicle. When you sell your car, the tax is automatically cancelled and any remaining months are refunded to you by DVLA. The new owner must tax the vehicle immediately. As a buyer, always verify the vehicle's tax status before purchasing.

Q: What is the luxury car tax threshold in the UK 2026?

The additional rate for vehicles over £40,000 (list price) adds £410 per year to standard VED rates for years 2-6 of registration. This surcharge brings the annual cost for high-emission vehicles over £40,000 to around £600-690 per year. Pure EVs under £40,000 pay zero VED.