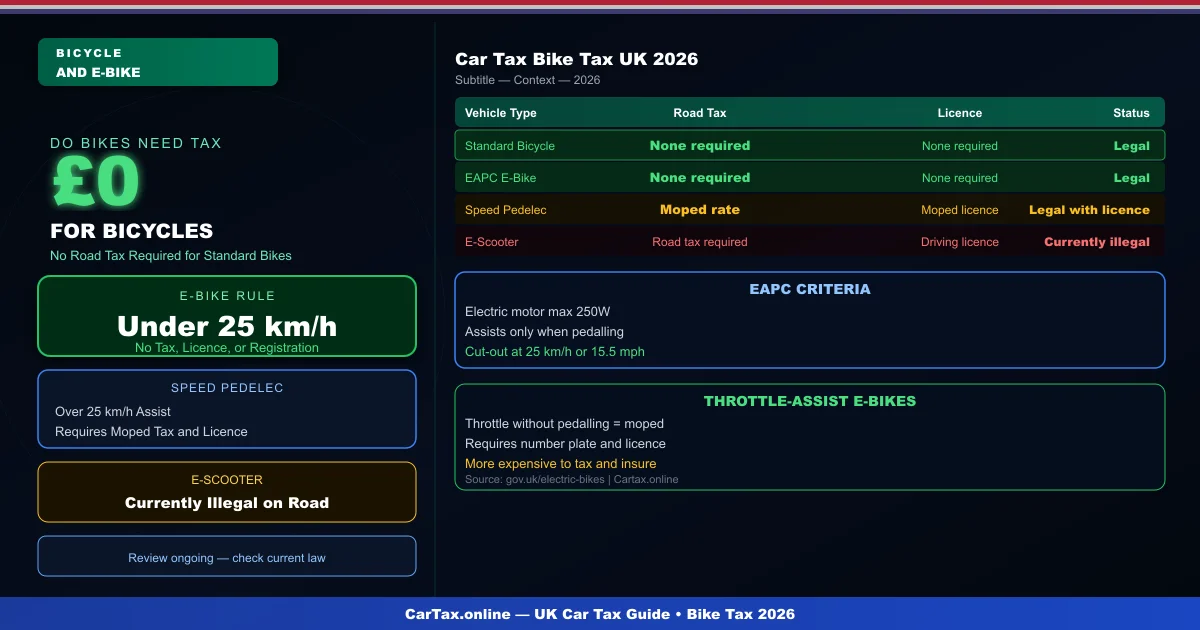

One of the most frequently asked questions about UK cycling is whether bicycles need road tax. Understanding the rules for standard bicycles, electric bicycles, and faster electric vehicles helps clarify the legal framework.

Standard Bicycles: No Road Tax Required

Standard pedal bicycles do not require road tax. By law, Vehicle Excise Duty applies only to motor vehicles — defined as vehicles propelled by mechanical means. A bicycle propelled solely by human power is not a motor vehicle and therefore does not require VED. You also do not need a driving licence or insurance to ride a standard bicycle on UK roads. However, you must obey road traffic laws and the Highway Code.

Electrically Assisted Pedal Cycles

Electrically assisted pedal cycles (EAPCs) — commonly known as e-bikes or pedelecs — are also exempt from road tax when they meet certain criteria. An EAPC is defined as a cycle with an electric motor that assists only while the rider is pedalling, with the assistance cutting out at 25 km/h (15.5 mph). If the cycle meets these criteria, it is treated as a pedal bicycle for tax and licensing purposes — no road tax, no licence, no registration required.

Speed Pedelecs and S-Pedelecs

Faster electric bicycles — speed pedelecs or S-pedelecs — that assist up to 45 km/h (28 mph) do not qualify as EAPCs. These are classified as mopeds or motorcycles depending on their power output and speed, and therefore require road tax, registration, and a licence to ride. A speed pedelec above 250W motor power and 45 km/h assistance is treated as a moped in the UK and requires VED, number plates, and an appropriate licence. Related: Car Tax and Bike Tax UK 2026 | Avoid This Common Car Tax Error That Costs GBP1K | Big Car Tax Changes Coming to UK 2026 | 5 Clever Ways to Tax My Car Online and Save Money.

Throttle-Assist Electric Bikes

Electric bicycles with a throttle that provides assistance without pedalling — even if the throttle cuts out at 25 km/h — do not meet the EAPC definition and are treated as mopeds. These vehicles require road tax, number plates, and a moped licence. This is an important distinction for buyers of electric bikes who may not realise their throttle-equipped bike is legally classified differently from a standard pedelec.

Electric Scooters

Electric scooters — self-balancing stand-on electric vehicles — are currently illegal to ride on UK public roads (as of 2026). They are classified as motor vehicles under the Road Traffic Act and require registration, road tax, and a driving licence. Private use on land may be permitted in some cases, but public road use requires full compliance. The law on e-scooters is under review, but no change to their legal status has yet been enacted.

Tax Implications for E-Bike Businesses

Businesses providing e-bikes to employees should understand that employer-provided EAPCs meeting the EAPC criteria do not incur a benefit-in-kind tax charge, while faster electric vehicles do. If a business provides a speed pedelec or S-pedelec to an employee, this counts as a company vehicle and may be subject to BiK tax. EAPCs meeting the 25 km/h criteria are specifically excluded from the BiK rules.

Official Resources: GOV.UK Check Vehicle Tax | GOV.UK Vehicle Tax | DVLA Online | MOT Check

Frequently Asked Questions

Q: How much is car tax (VED) in the UK 2026?

Car tax rates in the UK depend on your vehicle's CO2 emissions and list price. Standard rates start from £190 per year for petrol and diesel cars, with zero-rated VED for EVs. First-year rates vary from £0 to £2,605 depending on emissions. Additional premiums apply for vehicles over £40,000.

Q: How do I check if my car is taxed online?

You can check your vehicle's tax status for free on the Gov.uk website at gov.uk/check-vehicle-tax. You'll need your vehicle's registration number (number plate). You can also check via the Motor Insurance Database to verify road tax and insurance status simultaneously.

Q: Can I get a refund on car tax if I sell my vehicle?

Yes — if you sell or scrap your vehicle, you can claim a refund on any full months of remaining road tax. Contact DVLA with the V11 reminder letter or apply online at gov.uk. Refunds are usually processed within 4-6 weeks.

Q: Is road tax refund available when transferring ownership?

No — road tax does not transfer with the vehicle. When you sell your car, the tax is automatically cancelled and any remaining months are refunded to you by DVLA. The new owner must tax the vehicle immediately. As a buyer, always verify the vehicle's tax status before purchasing.

Q: What is the luxury car tax threshold in the UK 2026?

The additional rate for vehicles over £40,000 (list price) adds £410 per year to standard VED rates for years 2-6 of registration. This surcharge brings the annual cost for high-emission vehicles over £40,000 to around £600-690 per year. Pure EVs under £40,000 pay zero VED.