Car Depreciation Rate Under Income Tax Act 1961

The Income Tax Act 1961 prescribes specific depreciation rates for motor cars under Section 32. These rates apply to cars used for business purposes and determine how much deduction a business owner or self-employed professional can claim each year. Understanding these rates is essential for accurate tax planning and maximising your legitimate deductions when purchasing a car for commercial use.

In April 2026, the standard depreciation rate for motor cars in India remains at 15% per year under the Written Down Value (WDV) method. This rate has been consistent for several years and applies to all categories of motor cars not acquired on hire purchase. The WDV method is preferred by most businesses because it front-loads the deduction, giving larger tax savings in the early years of ownership.

Standard Depreciation Rates for Motor Cars

Under Section 32(1)(i) of the Income Tax Act, motor cars fall under the general block of assets taxed at 15% per year under WDV. This rate applies to the entire block of motor cars owned by a business. If you own multiple cars for business purposes, all of them are depreciated within the same 15% WDV block, and the total depreciation across all cars cannot exceed the block's written down value in any given year.

For motor cars acquired under hire purchase agreements, the depreciation rate is higher at 20% per year under WDV. This reflects the financing cost component embedded in hire purchase transactions. Businesses financing vehicles through HP need to track this distinction carefully as it affects the timing and amount of deductions claimed.

Under the Straight Line Method (SLM), the implied rate for motor cars is 11.88% per year, which produces the same total deduction as 15% WDV over the standard 15-year block life. Most businesses prefer WDV because it provides larger deductions in the early years, which is more valuable from a present-value tax-savings perspective.

Section 179 — Immediate Full Depreciation Deduction

Section 179 of the Income Tax Act allows businesses to claim 100% depreciation deduction in the year of acquisition for certain eligible assets. For motor cars specifically, Section 179 deduction was previously available but has been restricted in recent years. As of April 2026, the immediate full deduction under Section 179 is generally not available for motor cars except under specific circumstances related to electric vehicles and certain priority sectors.

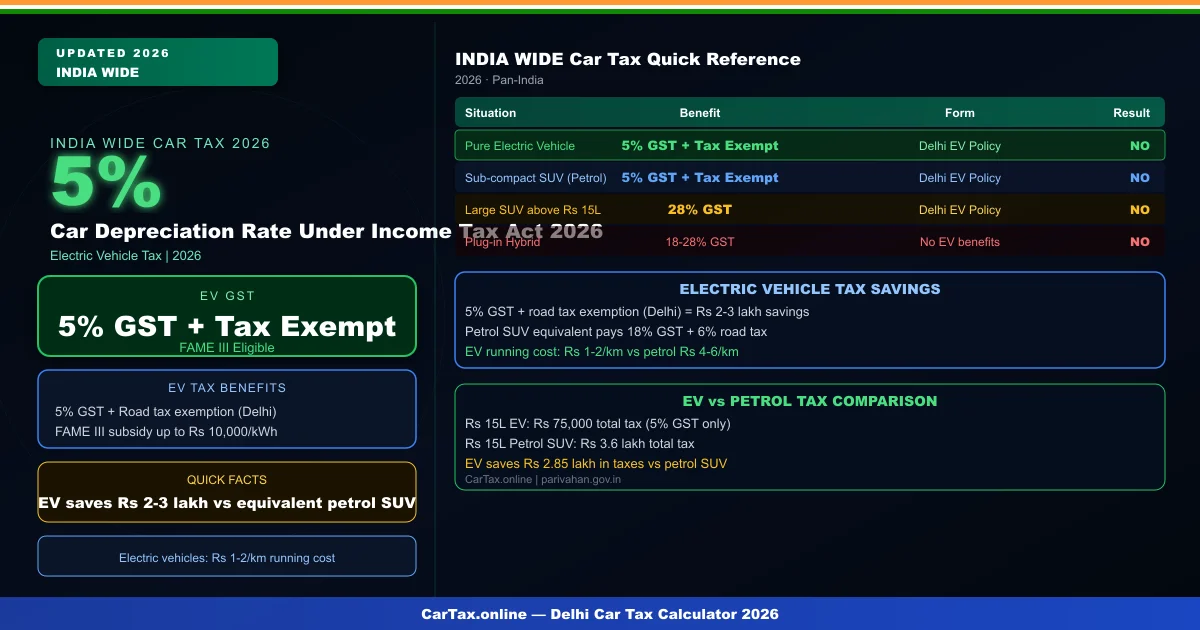

The more practically relevant Section 179 provision in 2026 relates to the additional depreciation that can be claimed in the first year. Beyond the standard 15% rate, businesses can claim an additional 15% depreciation of the cost of the car in the first year of acquisition. For electric vehicles used for business, the additional first-year depreciation is 30% instead of 15%, making EVs significantly more attractive from a tax perspective.

Additional First-Year Depreciation

Beyond the standard rate, businesses can claim additional depreciation in the first year of acquisition. This additional depreciation was introduced as an incentive for capital expenditure and is available for all tangible assets including motor cars used for business. The additional depreciation rate for most vehicles is 15% of the cost in the first year.

For electric vehicles, the additional first-year depreciation is doubled to 30% under the government's electric mobility push. This means a business purchasing an electric car at INR 10 lakh could claim up to 45% total depreciation in Year 1 (15% standard + 30% additional), resulting in a deduction of INR 4.5 lakh in the first year alone against an original cost of INR 10 lakh.

The combined effect of standard rate plus additional depreciation makes the first year the most valuable for car depreciation claims. Businesses timing their vehicle purchases strategically can optimise their annual tax liability by accelerating deductions into high-income years.

Block of Assets — How It Works

Income tax depreciation in India operates on the block of assets concept. Rather than depreciating each asset individually, assets of similar type are grouped into blocks. All motor cars form a single block taxed at 15% WDV. Each car you own for business falls into this block, and the total depreciation you can claim is limited to the written down value of the entire block.

The written down value of the block is calculated as: original cost of all cars minus accumulated depreciation claimed. If you sell a car, the sale proceeds are subtracted from the block's WDV, not from individual car values. If the sale proceeds exceed the block's WDV, the excess is treated as income under the head "Income from other sources."

If the block's WDV becomes zero, no further depreciation can be claimed on any remaining cars in that block. You must acquire a new car to restart the depreciation cycle for the block. This makes regular fleet renewal a strategic consideration for businesses with large vehicle fleets.

Car Depreciation Rate for Different Vehicle Categories

Not all vehicles are treated equally under the Income Tax Act. Motor cars specifically attract the 15% WDV rate. Goods vehicles (trucks, lorries) and buses attract a higher rate of 25% WDV, reflecting their heavier commercial use and faster depreciation in real terms. This distinction matters for businesses with mixed fleets.

Electric vehicles, while still categorised as motor cars for depreciation purposes, benefit from enhanced additional first-year depreciation at 30% instead of 15%. This policy incentive reflects the government's aim to accelerate EV adoption in commercial fleets. The standard 15% WDV rate still applies, but the enhanced additional depreciation makes the effective first-year deduction significantly higher.

Frequently Asked Questions

What is the standard depreciation rate for motor cars under Income Tax Act Section 32?

The standard depreciation rate for motor cars under Section 32(1)(i) of the Income Tax Act 1961 is 15% per year under the Written Down Value (WDV) method. This applies to all motor cars used for business purposes. Motor cars acquired on hire purchase attract a slightly higher rate of 20% WDV. The WDV method front-loads the deduction, giving larger tax savings in the early years of ownership compared to the Straight Line Method.

Can I claim 100% depreciation on a car under Section 179 in 2026?

Section 179 immediate full deduction is generally not available for motor cars in 2026. The primary first-year tax benefit for cars comes from additional depreciation of 15% of cost (30% for electric vehicles) on top of the standard 15% WDV rate. However, specific priority sector and electric vehicle incentives may provide enhanced first-year deductions. Consult a tax professional or refer to the latest Income Tax Act provisions for current eligibility.

What happens to depreciation when I sell my business car?

When you sell a car from your business block, the sale proceeds reduce the block's written down value (WDV). If proceeds exceed the block's WDV, the excess is treated as income taxable under "Income from other sources." If the block's WDV becomes zero before you acquire a replacement, no further depreciation can be claimed until a new car is added to the block. For businesses regularly renewing their fleet, timing sales and purchases carefully can prevent unexpected tax liabilities.

What is the depreciation rate for electric vehicles under Income Tax Act 2026?

Electric vehicles are categorised as motor cars and attract the standard 15% WDV rate. However, they qualify for enhanced additional first-year depreciation of 30% of cost (instead of 15% for petrol/diesel cars). This means total first-year depreciation on an EV can reach 45% of cost (15% standard + 30% additional). This policy incentive reflects the government's electric mobility push and makes EVs significantly more attractive from a tax planning perspective for businesses.

Are salaried employees eligible to claim car depreciation under Income Tax Act?

No. Car depreciation under Section 32 of the Income Tax Act is a business expense deduction. It is available only to self-employed individuals, businesses, and companies that use vehicles for commercial purposes. Salaried employees cannot claim car depreciation on their personal tax returns as it is not a personal tax benefit. If you are a salaried employee using a company-provided car, the perquisite value is added to your salary and taxed accordingly.