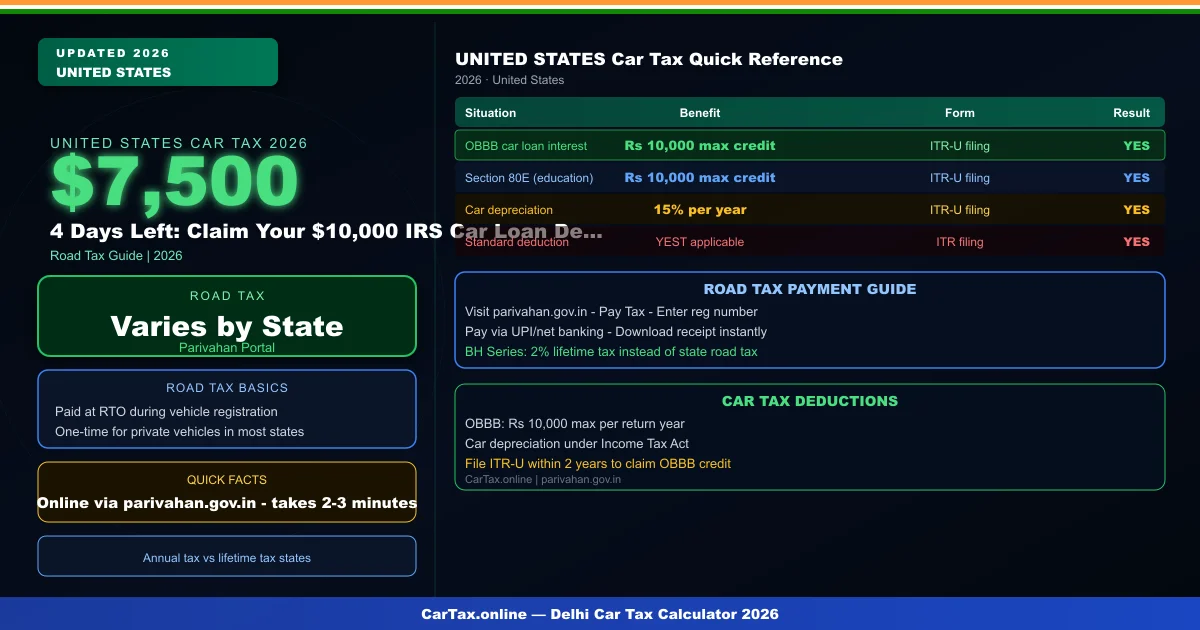

As of April 11, 2026 in the United States, the clock is ticking for millions of American taxpayers. The OBBB Act (Omnibus Business and Buildings Act) of 2025 introduced one of the most significant car-related tax deductions in recent memory: up to $10,000 in car loan interest deduction — claimable on Schedule 1-A, Line 11 of Form 1040. With only 96 hours remaining until the April 15 tax filing deadline, here is everything you need to know to claim this refund before it disappears.

What Is the IRS Car Loan Deduction on Schedule 1-A?

The OBBB Act 2025 introduced a above-the-line deduction for interest paid on car loans used for business purposes. Unlike most itemized deductions, this deduction reduces your taxable income directly — meaning it benefits you even if you take the standard deduction. The maximum deduction is $10,000 per year, making it one of the most valuable tax breaks for small business owners and self-employed individuals who use a vehicle for work.

Who Qualifies for the IRS Car Loan Deduction?

Not everyone can claim this deduction. The IRS has specific rules about both the taxpayer and the vehicle:

1. You Must Be Self-Employed or Running a Business

The car loan deduction is only available to self-employed individuals, sole proprietors, LLC members, and S-Corp shareholders who use a vehicle in their trade or business. If you are a W-2 employee, you cannot claim this deduction — even if you use your car for work purposes. Your employer would need to reimburse you through a separate arrangement.

2. Your Car Must Be Used for Business

You must use the vehicle at least 50% of the time for business purposes. Personal use does not disqualify you, but the deduction is proportionally reduced. If you use your car 60% for business and 40% personal, you can deduct 60% of the interest paid.

3. Income Limits Apply

The deduction phases out for taxpayers with modified adjusted gross income (MAGI) above $200,000 (single) or $250,000 (married filing jointly). Between $100,000 and $200,000, you receive a partial benefit. Below $100,000, you get the full $10,000 deduction.

How to Check If Your Car Qualifies (VIN Lookup)

One lesser-known requirement: the vehicle must be manufactured in the United States. The IRS checks this by looking at the first character of your Vehicle Identification Number (VIN):

- VIN starts with 1: Assembled in the United States (American Motors)

- VIN starts with 4: Assembled in the United States (General Motors)

- VIN starts with 5: Assembled in the United States (Chevrolet)

- Any other first letter: Foreign-manufactured — does not qualify for the full deduction

To find your VIN, look at the driver's side dashboard (visible through the windshield), the door jamb on the driver's side door post, or your vehicle registration documents.

IRS Car Loan Deduction — Who Can Claim? (2026)

| Taxpayer Type | Car Must Be | Max Deduction | Income Limit | Status |

|---|---|---|---|---|

| Self-Employed / Sole Proprietor | Business use 50%+ | $10,000 | $100k–$200k MAGI | YES ✓ |

| LLC Member or S-Corp Shareholder | Business use 50%+ | $10,000 | $100k–$200k MAGI | YES ✓ |

| W-2 Employee (Salary) | N/A | $0 | Not available | NO ✗ |

| Foreign-Manufactured Vehicle | VIN first letter not 1/4/5 | Partial only | Varies | LIMITED ⚠ |

Step-by-Step: How to Claim the Deduction on Form 1040

Follow these exact steps to claim your car loan interest deduction before the April 15, 2026 deadline:

Step 1: Gather Your Documents

- Form 1098 (Mortgage Interest Statement) from your lender — shows total interest paid

- Car purchase contract or loan agreement

- Vehicle title and registration showing the VIN

- Business use log (mileage tracker, mileage app, or handwritten log)

Step 2: Calculate Your Business Use Percentage

Divide the number of business miles by total miles driven in 2025. If you drove 20,000 total miles and 12,000 were for business, your business use percentage is 60%. Multiply your total interest paid by this percentage. If you paid $8,000 in interest and business use is 60%, your deduction is $4,800.

Step 3: Complete Schedule 1-A, Line 11

Download Form 1040 Schedule 1-A from IRS.gov. Enter the calculated interest amount on Line 11 — Other Adjustments. Attach the schedule to your Form 1040 when filing.

Step 4: File Electronically or Mail

The fastest way to file with this deduction is IRS Free File (for incomes under $87,000) or commercial software like TurboTax, H&R Block, or TaxAct. If mailing, send to the address for your state listed in the Form 1040 instructions.

What If You Miss the April 15 Deadline?

If you miss the deadline, you can still claim the deduction by filing Form 4868 for an automatic 6-month extension. However, any taxes owed will start accruing interest at the IRS failure-to-pay rate (currently 8% per year) from April 15. An extension gives you time but not relief from interest charges on underpayment.

Alternatively, if you missed the deadline entirely, you have up to 3 years to amend your return using Form 1040-X. You can amend 2025 taxes up until April 15, 2029.

IRS Official Resources

For the official IRS Schedule 1-A instructions, visit irs.gov/forms-instructions. For the OBBB Act text and eligibility details, refer to the Congress.gov legislative database. Use our USA Car Tax Calculator to estimate your total car costs including sales tax, registration, and fuel excise.

Frequently Asked Questions

Can I claim this deduction if I lease a car instead of financing one?

Yes — under the OBBB Act, the equivalent deduction for leased vehicles is the lease deduction, also claimed on Schedule 1-A. The limit is proportionally calculated based on the lease term and business use percentage. Consult IRS Publication 463 for the exact calculation method.

What if my car is used 100% for personal purposes but I have a business?

You cannot claim any car-related deductions if the vehicle is used 100% for personal purposes. The business use requirement is strict. You must have documented business miles to claim any portion of the interest or lease deduction.

Does the deduction apply to loans taken in previous years?

Yes — if you refinanced an existing car loan or took a new loan in 2025, the interest paid in 2025 qualifies. Prepaid interest and points on the loan may also qualify under certain conditions. Keep all loan statements from 2025.

Can my spouse and I both claim the deduction on a jointly-owned car?

Yes — if both spouses are self-employed or business owners and both have business use of the vehicle, you can each claim a proportional share of the interest. Each of you must meet the 50% business use threshold independently.