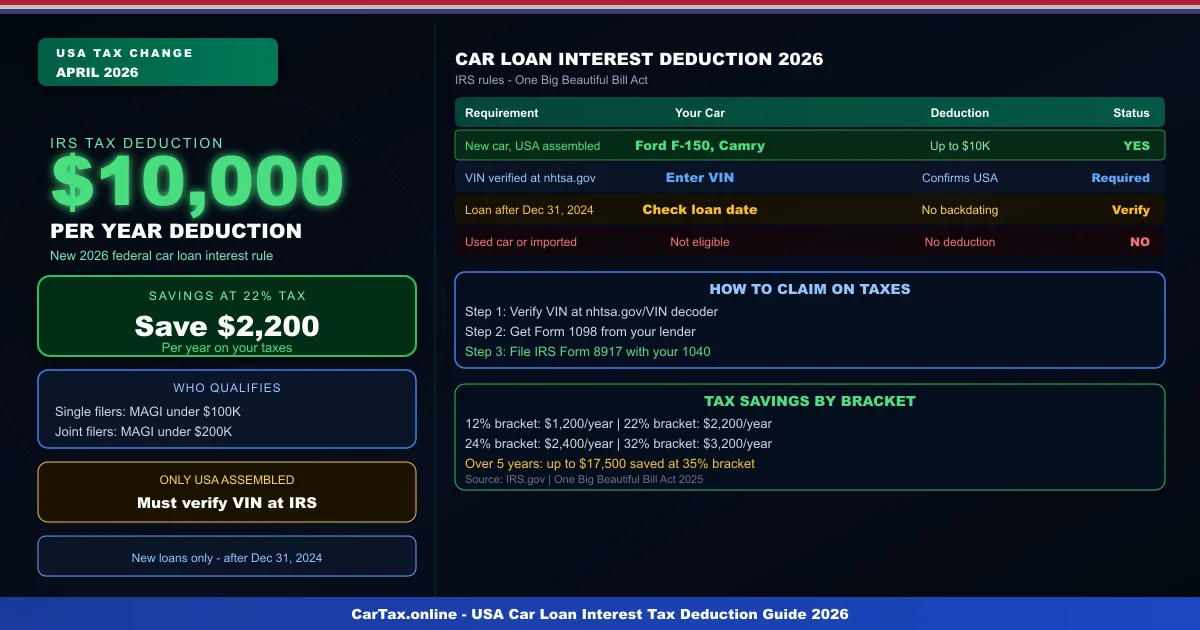

On April 22, 2026, the IRS confirmed one of the biggest tax changes for car buyers in decades. The new federal car loan interest deduction lets eligible taxpayers write off up to $10,000 in vehicle loan interest per year. If you financed a new car assembled in the USA after December 31, 2024, you could be sitting on a tax windfall worth thousands of dollars.

What Changed: The New Federal Deduction

For nearly 40 years, personal car loan interest was off-limits as a tax deduction. That changed when the One, Big, Beautiful Bill Act was signed into law. The provision called "No Tax on Car Loan Interest" creates a temporary deduction for interest paid on qualifying vehicle loans from 2025 through 2028.

Key facts about the deduction:

- Maximum deduction: $10,000 per year in interest

- Loan requirement: Must originate after December 31, 2024

- Vehicle type: New vehicles only (no used cars)

- Assembly requirement: Final assembly must be in the United States

- Vehicle weight: Gross vehicle weight rating under 14,000 pounds

- Availability: Tax years 2025 through 2028

This is not a tax credit that reduces the vehicle price at purchase. Instead, it is a deduction that lowers your taxable income by up to $10,000, saving you $2,200 annually if you are in the 22% tax bracket.

Crucial Note: Unlike mortgage or student loan interest, this is an above-the-line deduction — it reduces your adjusted gross income (AGI) directly. You do not need to itemize on Schedule A to claim it. This means even standard deduction filers benefit, making the car loan interest deduction 2026 one of the most accessible tax breaks in recent years.

Who Qualifies: Income Limits and Phase-Out

Income Thresholds

The car loan interest deduction is not available to everyone. The IRS phases it out based on modified adjusted gross income:

- Single filers: Deduction phases out above $100,000 MAGI

- Married filing jointly: Deduction phases out above $200,000 MAGI

- Phase-out rate: Reduction is proportional above the threshold

If your MAGI is below $100,000 (single) or $200,000 (married), you receive the full $10,000 deduction. Above these thresholds, the deduction shrinks gradually until it disappears entirely.

Tax Bracket Impact on Savings

The actual dollar savings depend on your tax bracket:

- 12% bracket: $10,000 deduction saves $1,200 per year

- 22% bracket: $10,000 deduction saves $2,200 per year

- 24% bracket: $10,000 deduction saves $2,400 per year

- 32% bracket: $10,000 deduction saves $3,200 per year

- 35% bracket: $10,000 deduction saves $3,500 per year

Over a 5-year loan, you could save $6,000 to $17,500 in total taxes depending on your bracket.

Qualifying Vehicles: USA Assembly Required

The VIN Check Rule

The most critical requirement is that your vehicle must have final assembly in the United States. You cannot claim the deduction with a simple declaration. The IRS requires you to enter the Vehicle Identification Number (VIN) on Form 8917 when filing your tax return.

The VIN tells the IRS exactly where the vehicle was assembled. If the last 11 characters of your VIN indicate final assembly in the USA, you qualify.

Quick VIN Reference

The first character (Position 1) of your VIN tells you the country of assembly:

- Starts with 1, 4, or 5: Assembled in the United States (Likely Qualifies)

- Starts with 2: Canada (may qualify if final assembly in USA)

- Starts with 3: Mexico (may qualify if final assembly in USA)

- Starts with J: Japan (Does Not Qualify)

- Starts with W: Germany (Does Not Qualify)

- Starts with K: Korea (Does Not Qualify)

Use the NHTSA VIN decoder at nhtsa.gov for a definitive answer on your specific VIN.

Vehicles That Typically Qualify

Many popular models assembled in the USA include:

- Ford: F-150, Mustang, Explorer, Bronco, Escape

- Toyota: Camry, RAV4, Corolla, Highlander (USA plants)

- General Motors: Silverado, Sierra, Tahoe, Suburban, Equinox

- Stellantis: Ram 1500, Jeep Grand Cherokee, Chrysler Pacifica

- Honda: Accord, CR-V, Civic (USA assembly)

Vehicles That Do NOT Qualify

- Any vehicle assembled outside the USA

- Used vehicles of any origin

- Demo cars and courtesy vehicles (they carry a title and are considered used)

- Certified Pre-Owned (CPO) vehicles (already titled as used)

- Motorcycles assembled abroad

- Vehicles with gross weight at or above 14,000 pounds

- Leased vehicles (not eligible — the lessor is the owner)

Important: Even low-mileage demo or courtesy vehicles do not qualify. If the vehicle has a title — even if never registered to a retail buyer — it is legally a used vehicle under IRS rules and does not meet the new vehicle requirement.

How to Calculate Your Deduction

Example: $35,000 Car at 7% Interest

Loan details:

- Purchase price: $35,000

- Down payment: $5,000

- Loan amount: $30,000

- Interest rate: 7%

- Loan term: 5 years

- Total interest paid in year 1: Approximately $2,050

At 7% over 5 years:

- Year 1 interest: $2,050 — full deduction claimed

- Year 2 interest: $1,720 — full deduction claimed

- Year 3 interest: $1,370 — full deduction claimed

- Year 4 interest: $995 — full deduction claimed

- Year 5 interest: $590 — full deduction claimed

Your total deduction over 5 years: approximately $6,725. At a 22% bracket, that is $1,480 in tax savings.

Example: $55,000 SUV at 8.5% Interest

Loan details:

- Purchase price: $55,000

- Down payment: $10,000

- Loan amount: $45,000

- Interest rate: 8.5%

- Loan term: 6 years

- Year 1 interest: Approximately $3,750

The interest exceeds the $10,000 cap, but you can only deduct up to $10,000. At a 24% bracket, that is $2,400 in tax savings for year 1 alone.

Step-by-Step: How to Claim the Deduction

Step 1: Verify Your Vehicle Qualifies

Before filing, confirm your vehicle was assembled in the USA:

- Find your VIN on the driver's side dashboard or door jamb

- Visit the NHTSA VIN decoder at nhtsa.gov

- Check the World Manufacturer Identifier (WMI) portion

- Confirm final assembly location is USA

Step 2: Gather Your Documents

- Form 1098 from your lender showing interest paid

- Vehicle purchase agreement showing VIN

- VIN verification documentation

- Loan documents showing origination date (after Dec 31, 2024)

Step 3: Complete IRS Form 8917

The deduction is claimed on IRS Form 8917, Vehicle Loan Interest Deduction. Enter your VIN, loan interest paid, and qualifying vehicle details. Attach the form to your Form 1040.

Step 4: Consider Estimated Tax Impact

If you expect to claim this deduction, you may want to adjust your W-4 withholding or make estimated tax payments to avoid underpayment penalties. Consult a tax professional for guidance.

Why This Changes Car Buying Decisions

Financing vs. Paying Cash

Historically, paying cash for a car made more sense because you avoided interest. Now, financing a qualifying USA-assembled vehicle can be more tax-efficient than paying cash, especially for expensive vehicles.

A buyer paying $50,000 cash saves interest but receives no deduction. The same buyer financing at 7.5% over 5 years pays approximately $9,750 in interest, but can deduct $9,750 (or the $10,000 cap, whichever is lower), saving $2,145 in taxes at the 22% bracket. The net cost of financing is reduced by the tax benefit.

American-Made Premium

The deduction creates a real financial advantage for USA-assembled vehicles over imports. A Toyota Camry assembled in Kentucky qualifies. A Toyota Camry assembled in Japan does not. This shift is already affecting showroom traffic patterns, with buyers asking about assembly locations before signing.

Calculate Your Savings

Use our Car Loan Interest Savings Calculator to see exactly how much you could save based on your vehicle price, interest rate, loan term, and tax bracket. Enter your details to find out whether financing beats paying cash, and how the deduction changes your effective cost of borrowing.

The Clock Is Ticking

The $10,000 car loan interest deduction expires after tax year 2028. Unless Congress extends it, vehicles purchased after 2028 will not qualify. If you are in the market for a new car, buying before the deadline locks in the deduction for your entire loan term.

Check your VIN today at the IRS website or nhtsa.gov to confirm your vehicle qualifies. The savings could be worth thousands of dollars on your next tax return.

Official IRS Resource: IRS guidance on car loan interest deduction

Disclaimer: This article is for informational purposes only and does not constitute tax advice. Tax laws are subject to change. Consult a qualified tax professional or CPA to determine your specific situation.