As of April 9, 2026 in the United States, with just 6 days left before the April 15 filing deadline, one of the most urgent tax questions Americans are searching right now is: is car loan interest tax deductible? The answer has changed significantly for 2025 returns. Thanks to a new provision in the One Big Beautiful Bill (OBBB), interest on auto loans for American-made cars is now deductible up to $10,000 — even for W-2 employees who do not itemize. On top of that, self-employed owners and business vehicle users have always been able to deduct car loan interest on Schedule C. This complete 2026 guide covers every scenario.

Is Car Loan Interest Tax Deductible in 2026? The Answer Has Changed

Historically, is car loan interest tax deductible had a simple answer for most Americans: no. Personal auto loan interest was classified as personal interest under the Tax Reform Act of 1986, making it non-deductible. Business vehicle interest was always deductible on Schedule C. But for 2025 tax returns (due April 15, 2026), there are now three separate paths where car loan interest can be deducted:

- Path 1 — OBBB personal deduction: Up to $10,000 in interest on loans for American-made cars — available to virtually all taxpayers, no itemizing required

- Path 2 — Business vehicle (Schedule C): The full business-use percentage of interest on a car used for self-employment or business — no dollar cap

- Path 3 — Combine both: If you are self-employed and drive an American-made car, you may be able to claim both — with coordination to avoid double-counting

The OBBB $10,000 Car Loan Interest Deduction — How It Works

Is interest on a car loan tax deductible without being self-employed? Starting with tax year 2025, yes — through the One Big Beautiful Bill auto loan interest provision. Here are the complete rules:

Who Qualifies

- Any U.S. taxpayer who financed an eligible vehicle and paid interest in 2025

- W-2 employees, retirees, and self-employed alike can claim this deduction

- You do not need to itemize — it is an above-the-line deduction on Schedule 1

- Income limits apply: the deduction phases out between $100,000–$150,000 (single) and $200,000–$250,000 (married filing jointly)

Which Cars Qualify

The vehicle must be assembled in the United States. The fastest way to check: look at your VIN (Vehicle Identification Number). The first character reveals the country of final assembly:

- 1 — United States ✓

- 4 — United States ✓

- 5 — United States ✓

- 7 — United States ✓

- 2 — Canada ✗

- 3 — Mexico ✗

- J — Japan ✗

Examples of qualifying vehicles: Ford F-150 (1FT), Chevy Silverado (1GC), Tesla Model Y (5YJ), Rivian R1T (7FC), Jeep Wrangler (1C4), Toyota Camry built in Georgetown KY (4T1), Honda Accord built in Marysville OH (1HG). See our full guide on American-made cars that qualify for the $10,000 IRS deduction.

How Much Can You Deduct

The deduction is capped at $10,000 of actual interest paid in 2025. Most buyers who financed a car in 2023–2024 at rates between 6.5%–8.5% will have paid $3,000–$8,000 in interest during 2025 — well under the cap, meaning the full amount is deductible. Only buyers with very large loan balances would approach or hit the $10,000 ceiling.

Where to Report It

Report the interest on Form 1040, Schedule 1, Line 24z (Other adjustments). You do not need Form 1098-VLI — the IRS has confirmed that the standard year-end interest statement from your lender is sufficient documentation for 2025 returns.

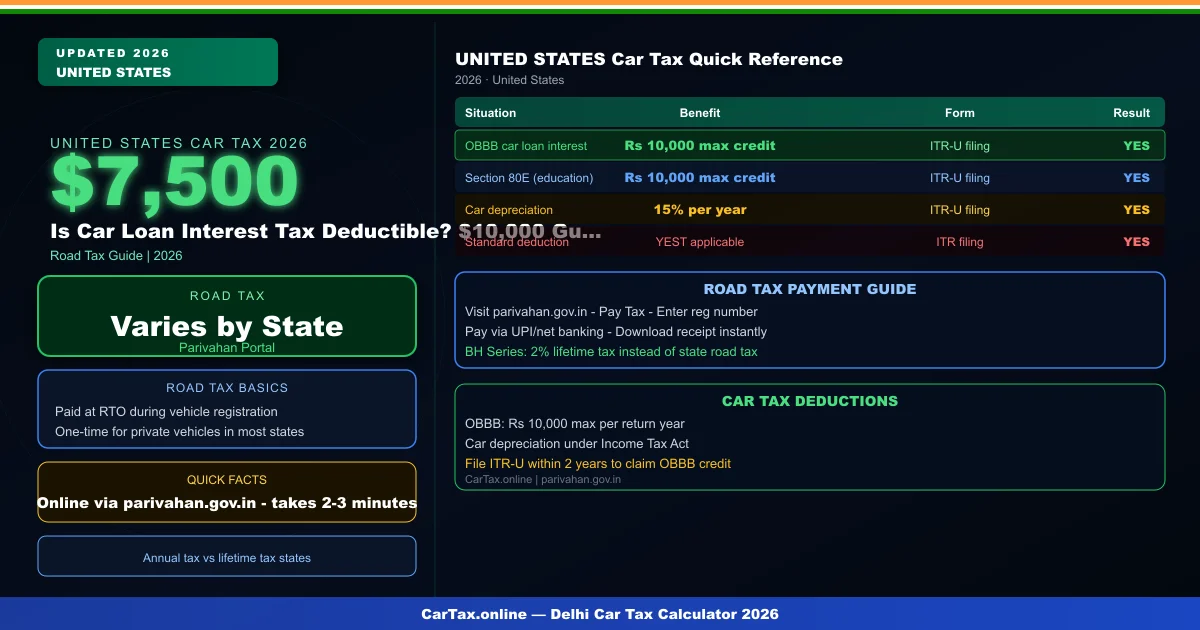

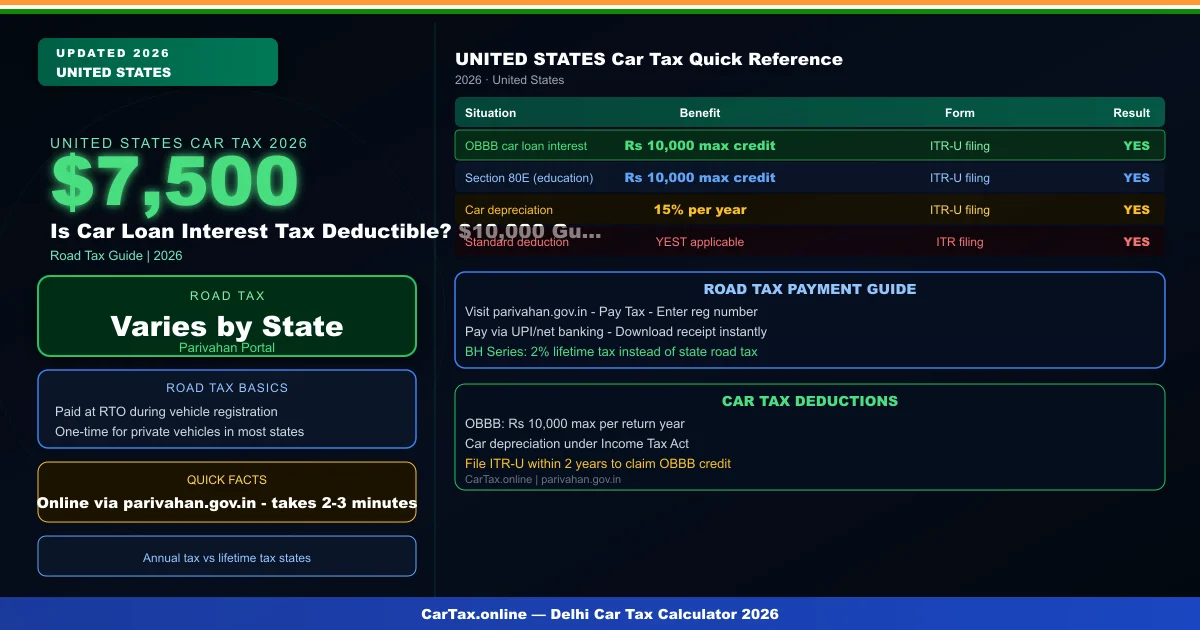

💡 Is Car Loan Interest Tax Deductible? Compare Your Situation

| Your Situation | Interest Deductible? | Where to Report | Max Deduction |

|---|---|---|---|

| Personal car loan — American-made (VIN 1/4/5/7) | Yes — OBBB new rule | Schedule 1, Line 24z | $10,000 |

| Business vehicle — self-employed / LLC | Yes — business % of interest | Schedule C, Line 16b | Unlimited |

| Self-employed + American-made (stack both) | Yes — both deductions | Sch C + Sch 1 | Best deal |

| W-2 employee — foreign-made car | No deduction available | None | $0 |

| Credit card interest (personal) | NOT deductible | None | $0 |

| Personal loan / unsecured debt | NOT deductible | None | $0 |

Is Interest on a Car Loan Tax Deductible for Self-Employed Workers?

Yes — and this has always been the case, long before the OBBB. If you are self-employed and use a vehicle for your business, is interest on a car loan tax deductible in the traditional sense? Absolutely — on Schedule C, Line 16b (Interest). Here is how it works:

- Actual expense method: You can deduct the business-use percentage of total interest paid. If the car is used 70% for business and you paid $6,000 in interest, the deductible amount is $4,200 on Schedule C.

- Standard mileage method: Interest is NOT separately deductible. Like car insurance and repairs, it is included within the per-mile rate.

- Mixed-use vehicle: The personal-use portion of interest is not deductible on Schedule C — but if the car is American-made, that personal portion may still qualify for the OBBB deduction on Schedule 1, Line 24z (up to $10,000 total combined).

Important: You cannot deduct the same dollar of interest on both Schedule C and Schedule 1, Line 24z. The business-use portion goes on Schedule C; the remaining personal-use portion may go on Schedule 1 under OBBB — coordinate carefully or ask your tax preparer to handle the split.

Is Car Loan Interest Tax Deductible for W-2 Employees? (Not Self-Employed)

Before the OBBB, the answer to tax credit car loan interest not self employed was a firm no. W-2 employees had no way to deduct personal auto loan interest under any provision of the tax code. The Tax Cuts and Jobs Act of 2017 eliminated the miscellaneous itemized deduction for employee business expenses (including vehicle costs) through 2025.

The OBBB changed this for 2025. Now, a W-2 employee who bought or financed an American-made car can deduct up to $10,000 in interest from their 2025 return — above the line, without itemizing. This is the first time since 1986 that personal auto loan interest has been deductible for the average American worker.

Example: A teacher earning $72,000 in 2025 who financed a Ford Explorer (VIN starts with 1FM) and paid $5,400 in loan interest can deduct the full $5,400 on Schedule 1, Line 24z. At the 22% tax bracket, this saves $1,188 in federal taxes — money back in their pocket by April 15.

Is the Interest on a Car Loan Tax Deductible for Leased Vehicles?

Leases are structured differently from loans — there is no interest in the traditional sense. Lease payments consist of a depreciation charge and a money factor (the lease equivalent of interest). For personal leases, no deduction is available under the OBBB, which specifically covers loan interest. For business leases, the lease payment (or its business-use percentage) is deductible on Schedule C, Line 20b as a rental/lease expense.

Is Credit Card Interest Tax Deductible?

Is credit card interest tax deductible? No — for personal purchases and balances, credit card interest is classified as personal interest under IRC Section 163(h) and is explicitly non-deductible. This has been the rule since 1986 and the OBBB did not change it. There is one exception: if you use a business credit card exclusively for business expenses and you are self-employed, the interest charged on business purchases is deductible on Schedule C, Line 16b.

This is a common source of confusion because the rules for auto loan interest (now partially deductible via OBBB) differ completely from the rules for credit card interest (still non-deductible). Keep these two categories separate when filing.

Is Personal Loan Interest Tax Deductible?

Personal loan tax deduction rules are the same as credit card interest: no deduction for personal-purpose loans. If you took out a personal loan (from a bank, credit union, or online lender) to buy a car, the interest on that personal loan is not deductible under the OBBB — the OBBB deduction specifically applies to auto loans (loans where the vehicle is collateral), not unsecured personal loans used to purchase a car. The distinction matters if your lender issued a personal loan rather than a traditional auto loan.

Mortgage interest is still deductible on Schedule A (up to $750,000 in loan principal for post-2017 mortgages). Student loan interest has its own above-the-line deduction (up to $2,500 on Schedule 1). But personal unsecured loans and credit cards remain non-deductible regardless.

Can You Write Off Car Payments? (Principal vs. Interest)

Can you write off car payments? Not the full payment — but the interest component is now deductible (under the rules above). Here is the breakdown:

- Principal repayment: Never deductible — paying down debt is not an expense

- Interest portion: Deductible up to $10,000 (OBBB, personal American-made car) or as a business expense (Schedule C)

- Full car cost deduction: The vehicle's purchase price can be deducted through depreciation, Section 179, or bonus depreciation if it is a business vehicle — this is separate from the loan payment itself

Your lender's year-end statement will show exactly how much interest vs. principal you paid in 2025. Many online lender portals (Toyota Financial, Ford Credit, Chase Auto, Capital One Auto Finance) have downloadable year-end interest statements available in the account portal now — download yours before April 15.

How Much Tax Do You Actually Save on $10,000 of Car Loan Interest?

The OBBB deduction is a deduction (reduces taxable income), not a credit (which would directly reduce your tax bill dollar-for-dollar). Your actual tax savings depend on your marginal tax bracket:

- 12% bracket (income $11,601–$47,150 single): $10,000 × 12% = $1,200 saved

- 22% bracket (income $47,151–$100,525 single): $10,000 × 22% = $2,200 saved

- 24% bracket (income $100,526–$191,950 single): $10,000 × 24% = $2,400 saved

- 32% bracket: $10,000 × 32% = $3,200 saved (but phase-out begins at $100K single)

If you paid less than $10,000 in interest (the typical case), the savings are proportionally lower. A buyer who paid $5,000 in interest and is in the 22% bracket saves $1,100. Use our USA Car Tax Calculator to factor the full cost of buying and financing a car — including state sales tax, registration, and now the OBBB interest deduction — before your next purchase.

How to Claim the Car Loan Interest Deduction Before April 15

With 6 days left until the April 15 deadline, here is the fastest path to claiming is car loan interest tax deductible on your 2025 return:

- Check your VIN: Log into your registration or find your VIN on the driver-side door jamb. If the first digit is 1, 4, 5, or 7 — you qualify for OBBB.

- Download your interest statement: Log into your auto lender's online portal (Toyota Financial, Ford Credit, Ally Auto, Capital One Auto, etc.) and download the 2025 annual interest statement or year-end account summary.

- Verify your income: If your AGI is above $100,000 (single) or $200,000 (joint), the deduction begins phasing out. Calculate your expected AGI first.

- Enter on Schedule 1: On Form 1040, Schedule 1 (Additional Income and Adjustments), enter your qualifying interest on Line 24z (Other adjustments). Write OBBB auto loan interest as the description if your tax software asks.

- File or extend: If you cannot complete your return by April 15, file Form 4868 for an automatic 6-month extension. Note: the extension extends your filing deadline, not your payment deadline — pay any estimated tax owed by April 15 to avoid penalties.

For the full IRS guidance on auto loan interest deductions and the OBBB provision, refer to the official IRS newsroom announcement at irs.gov/newsroom and IRS Publication 535 (Business Expenses) at irs.gov/publications/p535 for the Schedule C business interest rules.

Frequently Asked Questions

Is the interest on a car loan tax deductible if I refinanced in 2025?

Yes — if you refinanced and the vehicle is American-made (VIN starts with 1, 4, 5, or 7), the interest paid on the refinanced loan in 2025 still qualifies for the OBBB deduction. The key is the total interest paid during the calendar year 2025, regardless of how many loans or lenders were involved. Add the interest from all lenders' year-end statements together.

Can I claim car loan interest if I bought the car in 2025 but it was assembled in 2024?

Yes — the deduction is based on where the car was assembled, not when it was manufactured. If the VIN first digit is 1, 4, 5, or 7, the car qualifies regardless of its model year. A 2024 model year car purchased in 2025 with a qualifying VIN is fully eligible for the 2025 OBBB deduction.

Is car loan interest tax deductible for a car I use for both business and personal use?

Yes — but you need to split the deduction carefully. The business-use percentage of interest goes on Schedule C, Line 16b. The personal-use percentage of interest may qualify for the OBBB deduction on Schedule 1, Line 24z — but only if the car is American-made and your income is within the phase-out limits. Do not claim the same dollar of interest on both forms.

Is a car loan interest tax deductible if I bought a car for my LLC?

If the LLC is a single-member LLC taxed as a sole proprietorship, the interest goes on your Schedule C at the business-use percentage. If the LLC owns the car (title in the LLC's name), the interest is a business expense on the LLC's books. Either way, the business-use portion of car loan interest is deductible — and the OBBB personal deduction does not apply to vehicles titled in a business entity's name.