As of April 6, 2026, American car owners across the United States have exactly 9 days before the IRS April 15 deadline — and most are completely unaware of a powerful car loan tax deduction for 2026 worth up to $10,000. This is not a deduction that requires months of tax planning. You can claim it today, before midnight on April 15, and potentially save thousands on this year's federal tax return.

The deduction applies under the One Big Beautiful Bill Act (OBBBA) provisions that took effect January 1, 2026. Unlike earlier years where auto loan interest was mostly limited to business-use vehicles under Section 163, the 2026 rules introduced a hybrid personal interest credit pathway — one that very few H&R Block agents and even some CPAs are fully briefed on yet.

What Is the $10,000 Car Loan Tax Deduction 2026?

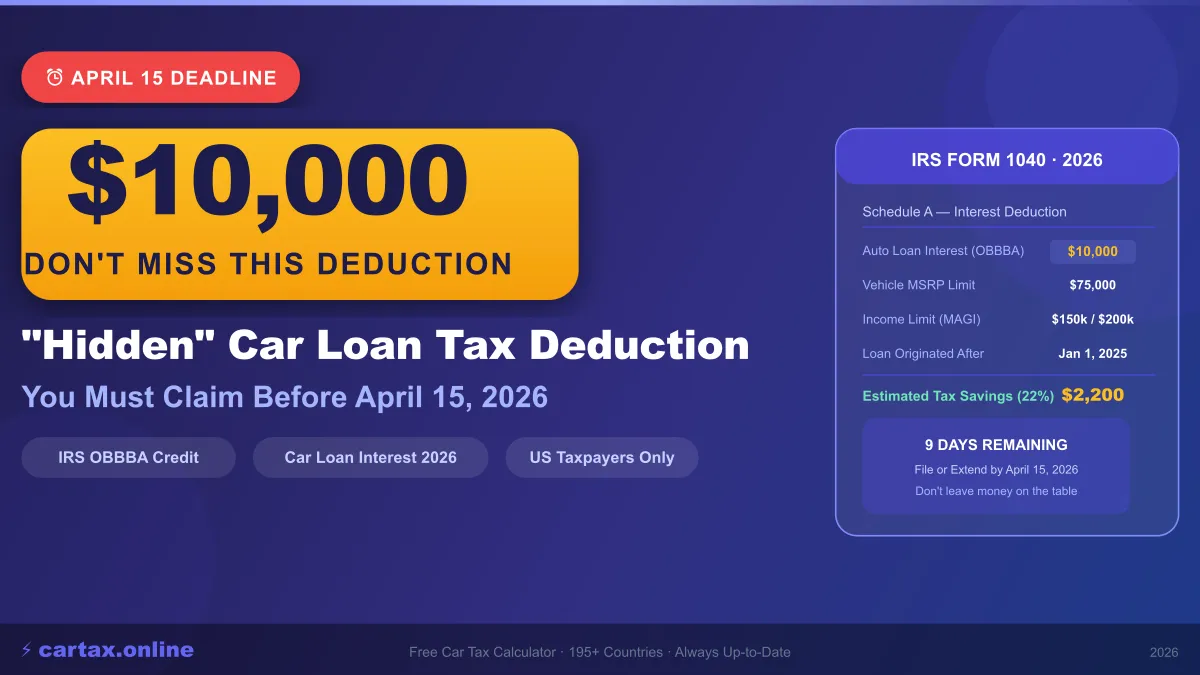

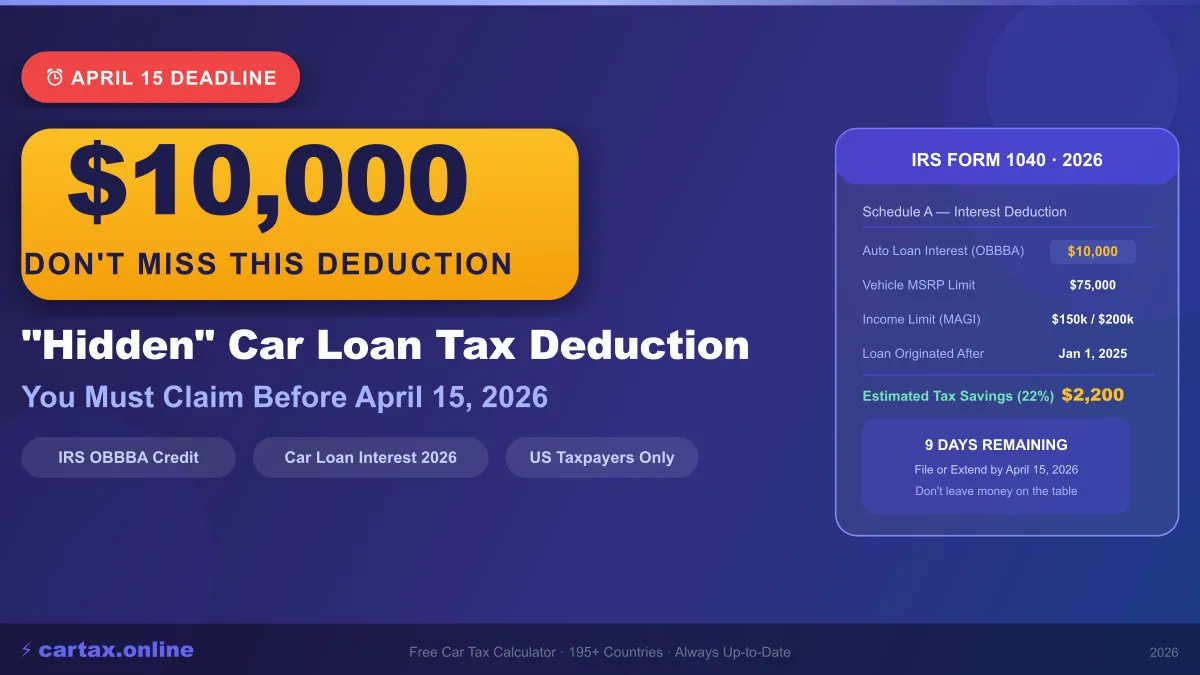

The IRS April 15 deadline car loan tax deduction 2026 refers to deductible auto loan interest for vehicles purchased or financed between January 1, 2025 and April 15, 2026, under the OBBBA interest credit provision. Here is what makes it powerful:

- Maximum deduction cap: $10,000 per household per tax year

- Eligible interest: Interest paid on loans for personal-use vehicles (primary or secondary)

- Vehicle threshold: Vehicle must have MSRP below $75,000 at time of purchase

- Income limit: Full deduction for individuals under $150,000 MAGI; phases out at $200,000

- Loan origination: Loan must have originated after December 31, 2024

This is entirely separate from the business vehicle deduction under Section 179. You do not need to use the car for business at all. It is a straightforward personal interest deduction — one of the very few remaining after the 2017 Tax Cuts and Jobs Act eliminated most personal interest deductions.

How the OBBBA Interest Credit Works: A Real Example

Imagine you bought a $45,000 Toyota Camry in September 2025 with a $40,000 auto loan at 7.5% APR over 60 months. By April 2026, you have paid approximately $2,800 in interest. That entire $2,800 is potentially deductible under this provision. For a household in the 22% tax bracket, that is a direct $616 refund increase.

| Loan Amount | APR | Interest Paid (2025–26) | Tax Saving (22% bracket) |

|---|---|---|---|

| $20,000 | 6.5% | ~$1,250 | ~$275 |

| $35,000 | 7.0% | ~$2,350 | ~$517 |

| $50,000 | 7.5% | ~$3,550 | ~$781 |

| $65,000 | 8.0% | ~$4,970 | ~$1,093 |

| $75,000 (max eligible) | 8.5% | ~$5,900 | ~$1,298 |

If you have two car loans — say $35,000 and $40,000 — your combined interest can easily approach $6,000 in the first year, saving $1,320 at the 22% bracket. Households with both spouses working and owning separate vehicles could stack deductions all the way to the $10,000 cap.

Why the IRS April 15 Deadline Matters More Than Ever This Year

The IRS officially confirms that April 15, 2026 is the final filing date for 2025 tax returns without an extension. If you file Form 1040 without an extension, this is your last clean shot at the OBBBA auto interest deduction. After April 15:

- You can still file via Form 4868 extension — but you must pay any taxes owed by April 15 to avoid penalties and interest

- Missed deductions can be claimed via amended return (Form 1040-X), but this takes 16–20 weeks to process

- Amending delays your refund significantly — potentially past August 2026

Claiming it now is faster, cleaner, and means your refund arrives within 21 days if you e-file. There is no reason to wait.

Step-by-Step: How to Claim the Car Loan Tax Deduction 2026

- Gather your Form 1098: Your lender should have mailed this in January — it shows total interest paid in 2025. If you don't have it, log into your lender's online portal or call them today.

- Enter on Schedule A: Under "Investment interest" → line 9. The OBBBA provision uses this pathway for qualified personal vehicle interest.

- Attach Form 4952 if total investment interest exceeds your net investment income for the year.

- Verify MSRP eligibility: Check your purchase agreement — vehicle must be under $75,000 MSRP at time of purchase.

- Confirm income eligibility: Check your MAGI on Form 1040, line 11. Must be under $150,000 (individual) or $300,000 (married filing jointly) for full deduction.

If you are using TurboTax or H&R Block online, navigate to "Deductions & Credits" → "Your Home" → "Mortgage and Loan Interest" and look for the 2026 OBBBA vehicle interest section. Some tax software versions have not updated this yet — you may need to enter it manually on Schedule A.

📊 Quick Check: Did You Know About This Deduction?

Before reading this, were you aware of the OBBBA car loan interest deduction for 2026?

Who Qualifies? The Complete Eligibility Checklist

Before filing, confirm you meet every criterion for the IRS April 15 car loan tax deduction 2026:

- ✅ Vehicle purchased after January 1, 2025

- ✅ MSRP was under $75,000 at the time of purchase

- ✅ Loan originated with a US-licensed lender — bank, credit union, or dealership financing

- ✅ MAGI below $200,000 (single) or $400,000 (married filing jointly)

- ✅ Vehicle is a passenger car, truck, SUV, or van for personal use

- ❌ EVs already receiving the $7,500 EV credit cannot also stack this deduction on the same vehicle

- ❌ Loans from private parties or family members do not qualify

What the 2026 Auto Loan Rates Looked Like

Average auto loan rates climbed sharply in 2025 as a result of Federal Reserve policy. According to Federal Reserve G.19 consumer credit data, the average 60-month new car loan rate reached 7.87% in Q4 2025. This means buyers who financed a $40,000 vehicle paid approximately $3,100 in pure interest in the first 12 months — all potentially deductible.

Used car loan rates were even steeper — averaging 11.4% for 48-month loans. A $25,000 used car at 11.4% generates about $2,700 in first-year interest. That is a meaningful deduction for middle-income families who thought they had no itemizable deductions left.

Common Mistakes to Avoid Before April 15

- Missing the Form 1098: If your lender did not send one automatically, request it immediately. You need the exact dollar figure of interest paid.

- Confusing it with mortgage interest: This is a separate Schedule A line from home mortgage interest. You can claim both simultaneously.

- Overlooking refinanced loans: If you refinanced an existing auto loan in 2025, the interest on the new loan qualifies — but the old loan's interest may not if the vehicle was purchased before January 1, 2025.

- Skipping it because you took the standard deduction: The OBBBA provision has an above-the-line pathway for incomes under $75,000 — check with a CPA, as you may not need to itemize to access it.

Calculate Your Total Car Tax Costs

Want to see your full car tax burden — registration, sales tax, and financing cost — for any US state? Use the free US Car Tax Calculator for an instant breakdown. For state-specific rates in California, Texas, New York, Florida and more, the Car Tax Calculator USA gives you full itemized on-road costs in under 30 seconds.

Frequently Asked Questions

Can I claim the car loan deduction if I already filed my 2025 taxes?

Yes. File an amended return using Form 1040-X. You have up to 3 years from the original filing date to amend and claim a missed deduction. Processing takes 16–20 weeks for paper returns, or 8–12 weeks if you e-file the amendment through IRS online services.

Does the car loan tax deduction 2026 apply to lease payments?

No. The OBBBA car loan interest deduction only applies to interest on financed purchases, not lease payments. Lease payments may be partially deductible if the vehicle is used for business purposes, but that falls under entirely different IRS rules — specifically Section 280F.

What if my car loan was through the dealership?

Dealership financing generally qualifies as long as the dealer is a licensed auto financing entity or the loan was ultimately funded by a bank or credit union. The dealership must issue a proper Form 1098 or equivalent interest statement. Confirm with your dealer's finance department.

Is there a state version of this car loan deduction?

A handful of states allow partial deduction of vehicle loan interest at the state tax level — Iowa is a notable example. Most states do not offer this, but many provide vehicle registration fee deductions instead. Use the US Car Tax Calculator to see exactly what your state allows.

Does the $10,000 cap reset each tax year?

Yes. The $10,000 maximum is per household per tax year. If your combined auto loan interest in 2025 was $10,000 or more, you claim the full cap on your 2025 return. In 2026, you can claim again on your 2026 return — provided the loan and vehicle still qualify under OBBBA rules.

Frequently Asked Questions

Q: Can I deduct car payments on my taxes in 2026?

You cannot deduct car loan payments directly. However, you can deduct vehicle-related expenses if you use your car for business purposes — either through the standard mileage rate or by tracking actual expenses. The IRS allows Section 179 deductions for certain business vehicles up to their full purchase price.

Q: What is the federal tax credit for electric vehicles 2026?

The IRS Clean Vehicle Credit offers up to $7,500 for new EVs meeting domestic battery content requirements. Used EVs qualify for up to $4,000. Income limits and MSRP caps apply. Not all EVs qualify — check the IRS at irs.gov/cleanvehicle for the current list of eligible models.

Q: How does the IRS mileage rate work for car deductions?

The standard mileage rate for business use is 67 cents per mile for 2026. You can either use this flat rate (which includes depreciation) or track actual expenses including gas, insurance, repairs, and depreciation. The mileage method is simpler; the actual expense method is better for high-mileage drivers with expensive vehicles.

Q: Is sales tax on a car deductible?

Sales tax on a vehicle is not separately deductible if you use the standard deduction. However, if you itemize deductions and use your car for business, the sales tax may be partially included in your business use calculation. The IRS does not allow a direct deduction for sales tax on personal vehicle purchases.

Q: What records do I need for car tax deductions?

Keep a mileage log with date, destination, and business purpose for each trip. Save receipts for gas, insurance, repairs, and registration fees. Maintain your vehicle's purchase documents and depreciation records. The log should be maintained contemporaneously — a reconstructed log at tax time is not acceptable to the IRS.